Meet the Woman who Went from Blasting Rocks to Making a Killing on Crypto

Jana, widely and rightfully regarded as the Crypto Queen, lives a blast—literally and figuratively. Interesting? Well, it is. For context, she worked as a blasting engineer, overseeing explosive detonations in mining operations. “My job was to make sure that the rocks wouldn’t fly too far during explosions,” Jana recalls. “There’s an intense level of responsibility and focus in that line of work, and I thrived on it.”

But while the blasts she controlled were meant for mining, life had other explosive turns waiting for her.

At age 10, she had always aspired to be an engineer. She put in colossal amounts of effort day in and day out, excelling in school, outperforming her peers. At a very young age, she was driven, not letting anything get in the way of achieving the dream. And she did.

Now, here’s the plot twist that nobody saw coming—as she was living the life she envisioned for herself as an engineer, she ended up feeling trapped by a rigid organization that often disregarded ethics for profit. After years, Jana ultimately made an audacious decision—she quit.

“Since I was ten, I wanted to be an engineer. But I didn’t get this far to just follow orders and ignore my values,” she shares. But leaving the only world she had ever known did not come easy at all.

She was lost—mentally, emotionally, and professionally. It wasn’t until her husband introduced her to the intimidating, volatile, and male-dominated cryptocurrency sector. Initially sceptical, even dismissive of cryptocurrencies and blockchain, she eventually found herself drawn in—not by the promises of overnight wealth but by its fascinating intricacies and the sense of community.

“I started by helping out in Discord servers, just hyping up conversations, keeping things lively. No one even knew who I was or that I was a woman,” Jana laughs. “But the more I stayed, the more I realized how vast and powerful this ecosystem was. It was like finding a whole new world where I could rebuild myself.”

Soon enough, Jana fully immersed herself and mastered every aspect of it. Because of her constant self-study and countless hours in online communities, she transformed from a curious outsider into a respected, renowned, and applauded leader. She embraced the challenges, overcame the barriers, and earned her title as the iconic and legendary Crypto Queen.

So how does she feel now? “I love it when I captivate people to look at me and listen to me and instantly realize I am a lot more than my appearance. I think I’m really good at helping people understand complicated things in a simple, genuine way. That’s what people love most about how I explain crypto.”

Trailblazing Women: H.E. Alia Bint Abdulla Al Mazrouei, Minister of State for Entrepreneurship, UAE Ministry of Economy

This article is part of a series entitled “Trailblazing Women” by Entrepreneur Middle East in celebration of International Women’s Day 2025.

The UAE has been taking incredible care of its female citizens and residents, lifting them up in their many personal and professional roles through its endless capacity for progress and empowerment. Just recently – in January 2025 – the UAE Ministry of Economy implemented a ministerial decision mandating private joint-stock companies in the UAE to allocate at least one seat for women on their boards of directors after the completion of the current board’s term.

It is one of the many decisions of H.E. Alia Bint Abdulla Al Mazrouei, Minister of State for Entrepreneurship, UAE Ministry of Economy, to open up the closely guarded doors of business leadership to women and recognize their contributions to the country’s economic development. “The UAE has long been at the forefront of gender equality in the region, particularly in the work- force,” says H.E. Al Mazrouei.

With a string of impactful executive roles to her name prior to being appointed to her current position in July 2024, including being the CEO of the Khalifa Fund for Enterprise Development, Advisor to the Chairman at the Abu Dhabi Department of Economic Development, Director General of the Human Resources Authority (HRA) in Abu Dhabi, and Director General of the Abu Dhabi School of Government (ADSG), H.E. Al Mazrouei is particularly eager to nurture new female talent, especially Emirati talent. “In a world where the role of women is continually evolving, Emirati women are making significant strides,” she adds.

In 2024, the UAE witnessed several milestones that highlight the success of the UAE’s policies to empower and build the capacities of Emirati women. Notably, the UAE advanced to the 7th place globally and retained its top regional position in the UN Gender Equality Index 2024, issued by the United Nations Development Program (UNDP). Furthermore, the Emirati Talent Competitiveness Council and the UAE Gender Balance Council signed an agreement to enhance Emirati women’s participation in the private sector through joint initiatives and programs. “The total count of business licenses in the UAE held by Emirati women account for more than 10% of total licenses,” H.E. Al Mazrouei proudly states.

She adds, “Women’s representation in the UAE government increased with the appointment of Sana bint Mohammed Suhail in December 2024 as Minister of Family, following the establishment of the new ministry.”

In this context, the Ministry of Economy and the General Women’s Union signed a cooperation memorandum to improve communication and unify efforts aimed at advancing economic empowerment and strengthening women’s roles in sustainable economic development. “The agreement aims to advance the economic empowerment agenda and strengthen the role of women in sustainable economic development, one of the distinguishing features of the UAE’s inspiring model for women’s empowerment,” H.E. Al Mazrouei explains. “This partnership focuses on increasing the participation of women entrepreneurs in commercial activities and promoting their economic contributions both locally and regionally.”

H.E. Al Mazrouei adds that the General Women’s Union also launched the second phase of the Women’s Economic Empowerment Program, aimed at equipping Emirati women with skills in various sectors, particularly entrepreneurship, supporting them to start up or expand their businesses.

H.E. Al Mazrouei’s support to enterprising women, and particularly Emirati women, traces back to the beginnings of her career when she was Group Chief Operating Officer of Mazrui International LLC, which was estab- lished by her family 50 years ago and grew into a Abu Dhabi-based conglomerate with a highly diversified business portfolio.

Due to her diverse professional experience, H.E. Al Mazrouei has a thorough understanding of how to support women’s professional advancement, effectively. “Firstly, it is important to promote awareness on gender biases through training programs for leaders, managers, and employees can help address these stereotypes,” H.E. Al Mazrouei says. “Establishing clear metrics for performance and focusing on merit-based promotions rather than personal biases will ensure that women have equal opportunities to rise in economic leadership.” She also advises creating women-focused networks and mentorship programs within organizations. “Encouraging senior women leaders to mentor younger women also helps to create a supportive ecosystem for career development. As an entrepreneur myself, I really believe that we have the ability to connect with and inspire other women who are keen to follow this path,” she explains. Thirdly, H.E. Al Mazrouei encourages transparent pay structures and equal pay for equal work policies. “Regular pay audits can ensure fairness, and companies should actively work to close the pay gap through policy changes and proactive recruitment strategies,” she says.

And lastly, H.E. Al Mazrouei supports educational and awareness campaigns that challenge traditional gender norms and highlight the importance of women’s participation in the workforce can gradually change societal attitudes. “Encouraging men to become allies in advancing gender equality and supporting women in leadership roles is also important,” she concludes.

H.E. Alia Bint Abdulla Al Mazrouei, Minister of State for Entrepreneurship, Advises Women in the UAE

Embrace innovation “Always be curious, explore new ideas, and embrace the latest technologies. The UAE’s rapidly changing market thrives on those who dare to innovate and adapt. Don’t be afraid to dream big and push boundaries – your creativity is your greatest asset.”

Build a strong network “No one succeeds in isolation. Surround yourself with fellow women entrepreneurs, mentors, and industry leaders who can offer guidance and support. Your network is more than just connections – it’s a community that can open doors to collaborations, funding, and the wisdom you need to grow. Together, we can achieve more than we ever could alone.”

Leverage government support “The UAE government offers a wealth of incentives, grants, and programs designed to support women entrepreneurs. These resources are there to help them turn their vision into reality, so take full advantage of them. They’re a testament to the UAE’s commitment to nurturing its women business leaders.”

Marketing Maven: Ziad Melhem, Chief Marketing Officer, CFI

CFI has become a significant force in the online trading sector, offering traders seamless access to global and local markets with a physical presence in 15 countries and five continents. Plus, the online trading provider is globally regulated and locally trusted with 14 licenses from reputable regulatory bodies. It should not then come as a surprise that it is a go-to choice of traders around the globe – its clients’ quarterly trading volumes on the platform exceeds US$1 trillion- just in Q4 2024, CFI saw a 27% increase from Q3 in active clients, and a 39% increase in client funding. The company’s commitment to technological innovations, financial literacy, and partnerships with globally renowned icons positioned it as a leader in the competitive trading industry.

However, knowing that even the best of products still need to be properly marketed to the right audiences at the right time and place, we caught up with Ziad Melhem, Chief Marketing Officer, CFI, to learn how he has managed to enhance CFI’s brand reach and truly engage and captivate audiences around the world.

Melhem’s approach starts with clearly defining marketing objectives- market expansion, customer engagement, and delivering cutting-edge technological solutions. “Firstly, our market expansion objective is divided into two parts,” he explains. “If it’s a new market we’re penetrating and aim for having the biggest market share in that particular market, we have a special playbook that we apply. Usually, the strategy is more challenging but exciting. At the same time, in other markets where we already have the biggest market share, it’s about expanding our existing presence as well as solidifying it further.” The second point, Melhem continues, relates to regularly enhancing customer engagement. “For existing clients, it’s about strengthening, nurturing, and retaining that relationship,” he says. “For new clients, we aim to establish a connection and retain it in the long term. This usually happens through our content marketing channels.”

Melhem reiterates that CFI offers comprehensive market access with more than 15,000 instruments, enabling traders to access leading platforms and tools, such as CFI Trading App and Webtrader, MT4, MT5, C-Trader, CFI MultiAsset, TradingView, among others, and proprietary tools integrated with AI-driven solutions, like Kaiana AI. All this innovation serves the company’s ultimate vision – to be the go-to brand for all things trading and investing, enabling financial inclusion by empowering everyone to achieve their financial goals, no matter their level of knowledge or experience.

“My third marketing objective is therefore about delivering technology and innovation, and it’s maybe a bit weird to hear a marketing person talking about the product, because it is not us who built it, but it is us who package this technology and innovation and deliver it to the customers,” Melhem explains. “It is us who make sure that the user experience is always enhanced. It is us who highlight the features of this technology and innovation to enable the users to use the best user experience as well as the best services.”

Now, how do these strategic marketing goals align with the broader business strategy of CFI? “I think it’s beyond alignment even, but that these goals are actually married to our broader, global business strategy.”

Related: Charting The Future: Hisham Mansour, Co-Founder And Managing Director, CFI

In achieving these objectives, CFI often resorts to out of home campaigns, such as “Beyond Trading” that highlighted the comprehensive services CFI offers beyond just trading, “Drive Your Success” that featured Lewis Hamilton to draw a parallel between the precision and excellence required in Formula 1TM racing and the rigorous standards CFI upholds in its trading services, and “More and Better” that reinforced the brand’s positioning by highlighting its superior offerings in online trading and financial services. “Personally, I’m a big fan of out of home campaigns, because I consider them a cornerstone of any 360 degrees marketing strategy,” Melhem says. “I think that the way people consume out of home campaigns is really natural because it just happens within the flow of their lives. Like if you’re driving, riding a bike, jogging, or walking in the mall, you consume these ads easily without being interrupted. If you look at other mediums, like digital ads for example, most of the time you get interrupted by an ad.”

Source: CFI

The creative process behind CFI’s out of home campaigns relies heavily on the deep understanding of client needs and the market itself. “If we get a solid grasp those, everything else becomes much easier, because from there it’s all about aligning our brand goals and brand messaging with the audience/market needs in order to come up with these bold creative campaigns.”

Source: CFI

The company’s messaging is enhanced through strategic alliances, such as with Lewis Hamilton, AC Milan, and top institutions (FIBA WASL, Department of Culture and Tourism of Abu Dhabi, Jordan Basketball Federation, Jordan Football Association, Lebanese Basketball Federation), that are aimed at reinforcing CFI’s commitment to world class standards. “For example, in our recent two campaigns, we worked our global brand ambassador, Lewis Hamilton, seven times F1 World Champion, to stress on our shared values – we’re talking about trading like a champion, about success, resilience, advancement, execution, precision, and so on,” Melhem explains. ” And we also use our local or regional partnerships, for example with the Department of Culture and Tourism Abu Dhabi, to deliver certain messages. These include that we are contributing to the community where we’re based. This actually has been very helpful for us and we will continue to do that in the future.”

CFI’s 360 degree campaigns cover key countries with an objective that its appealing branding message is visible to people through the main central touch points, from major airlines to main central roads. “When it comes to the locations, we’re very selective,” Melhem concludes. “We target premium locations, and I’m a big believer that the location passes its exclusive value to the brand itself, meaning that you cannot display your campaigns anywhere.”

Related: The 100: Hisham Mansour, Co-Founder and Managing Director, CFI

New Lucidity Insights Report Highlights the Middle East as a New Global Fintech Contender

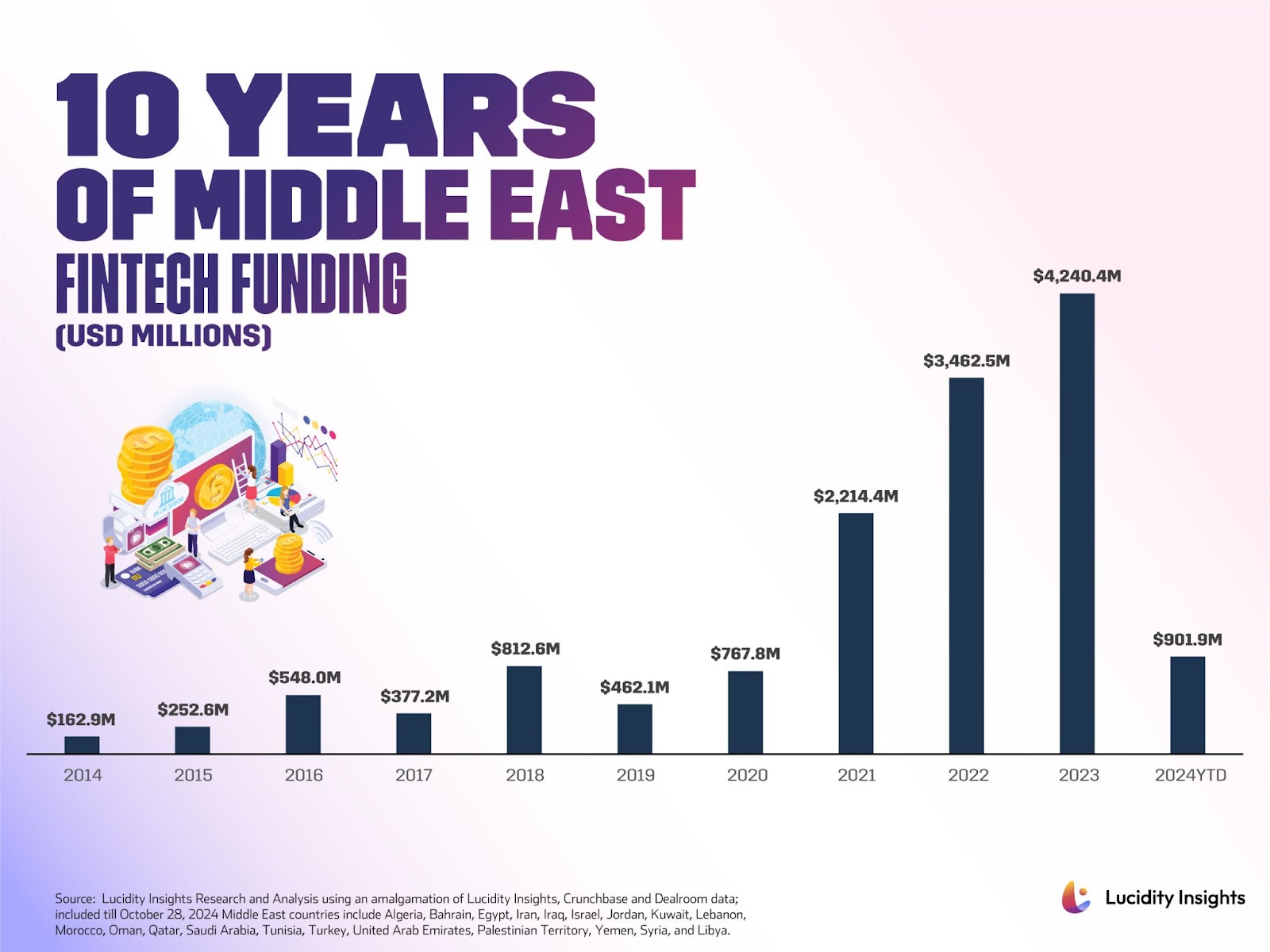

The Middle East’s fintech sector is on the rise. With over 1,500 fintech startups, a staggering US $4.2 billion in funding raised in 2023, and 7 IPOs and 30+ M&A exits since 2022, the Middle East region is emerging as a growing region for fintech innovation and investments. These achievements are no accident—they mark the culmination of a decade of strategic investments, bold entrepreneurial ventures, and supportive government policies.

Lucidity Insights’ latest special report in partnership with SAP, titled “The State of Fintech in the Middle East,” deep dives into this remarkable transformation. Discover the key players, emerging trends, and market forces shaping the future of finance in the MENAT (Middle East, North Africa, and Turkey).

A Decade of Fintech Growth and Momentum

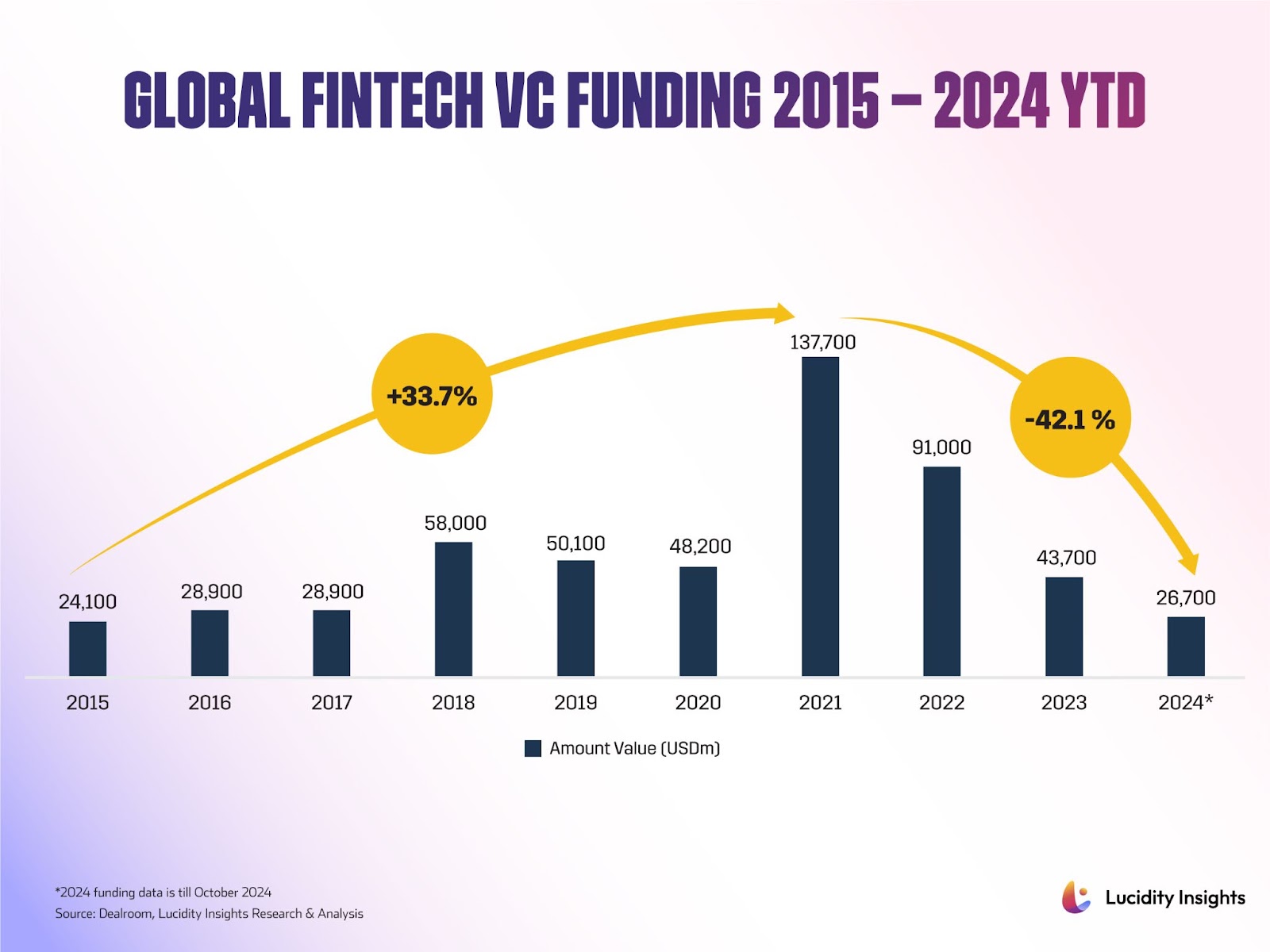

Globally, fintech has dominated venture capital flows, attracting over US $500 billion in funding since 2015. While global fintech funding peaked in 2021 at US $137.7 billion, the Middle East’s trajectory has been more consistent, culminating in a record US $4.2 billion in 2023, even amid global market cooling.

This sustained growth has fueled the rise of standout startups such as Tabby, a UAE-born BNPL unicorn now valued at US $1.5 billion, and Tamara in Saudi Arabia. Other regional leaders, including MNT-Halan, continue to attract significant investor interest, with funding trends pointing to a bright future for the ecosystem.

Unicorns in the Making

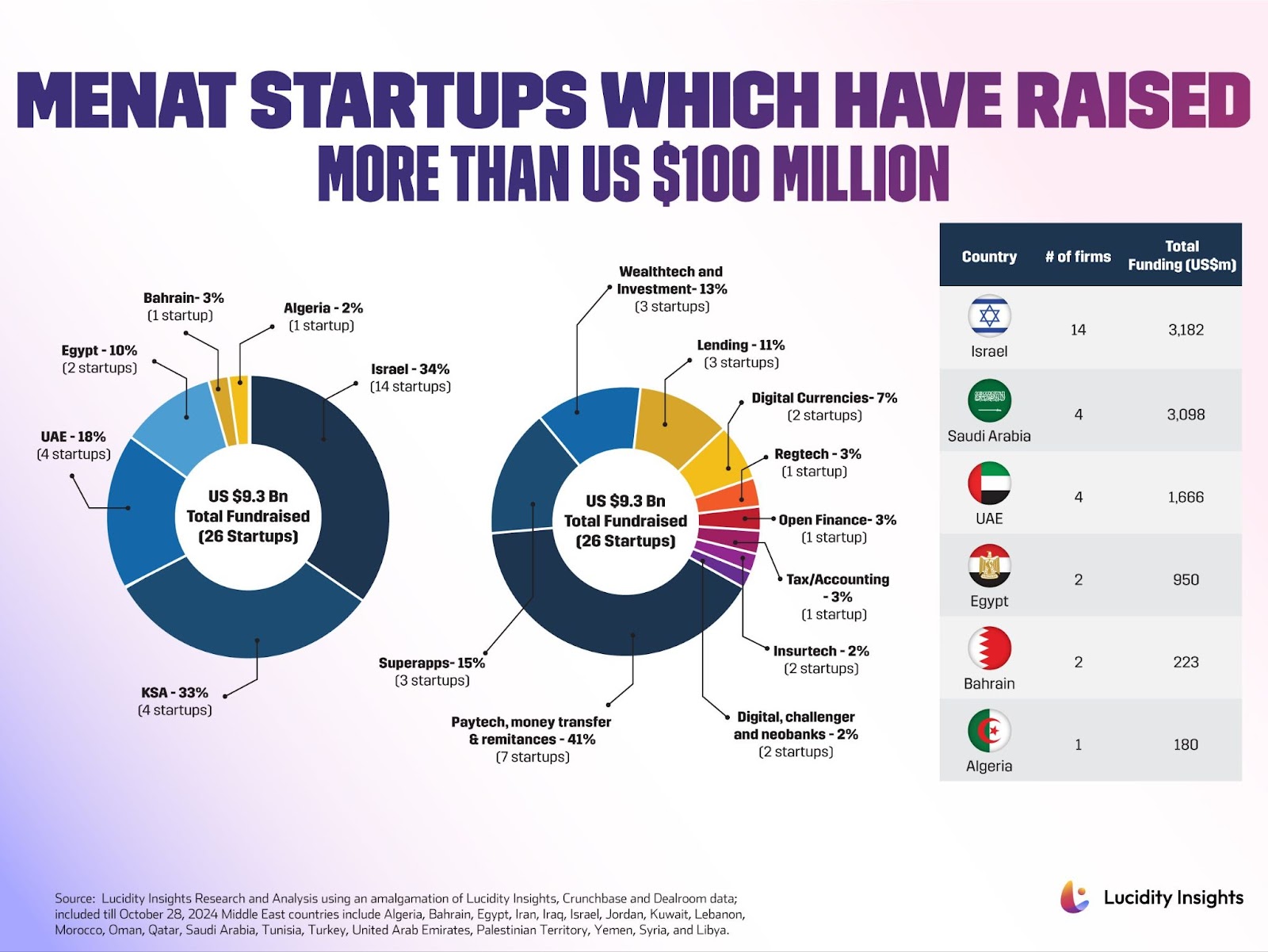

While global fintech giants like Stripe, Revolut, and Nubank dominate valuations, the Middle East is building its own unicorn pipeline. Startups like Geidea, Midas, PayTabs, and Sarwa are on the brink of unicorn status, joining the ranks of Tabby and Tamara.

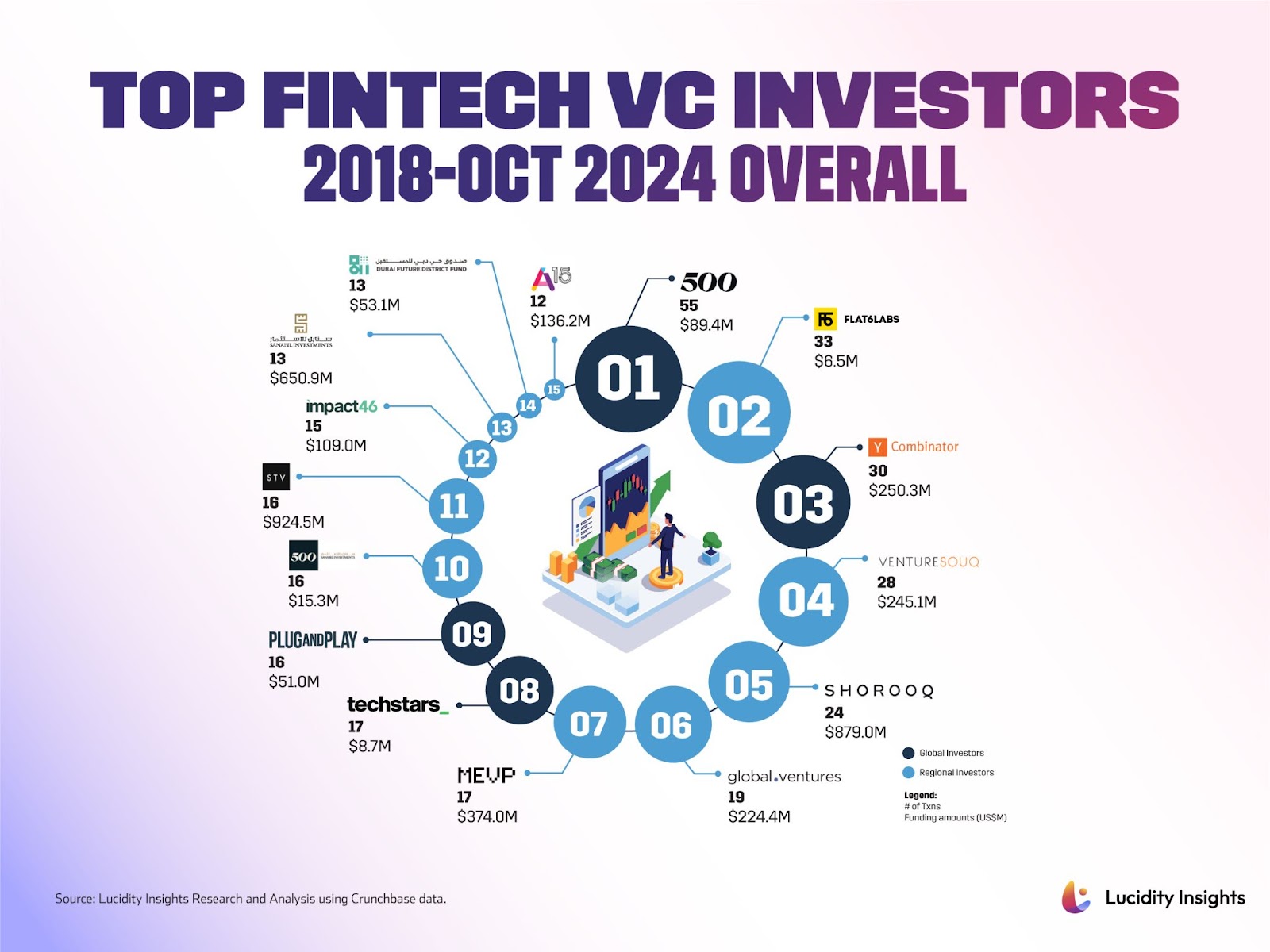

According to the Lucidity Insights‘ report, 26 MENA-based fintechs have already raised over US $100 million, signaling a robust pipeline of future unicorns. Notably, STV, a leading growth-stage Venture Capital fund based in Saudi Arabia, has invested US $924 million across 16 fintechs since 2018, showcasing the region’s growing investor confidence.

Even global players are taking notice: Y-Combinator has invested in 30 fintechs across the region, pouring in over US $250 million collectively in the last six years. This influx of capital underscores the region’s rising prominence on the global fintech stage.

Key Investment Sectors

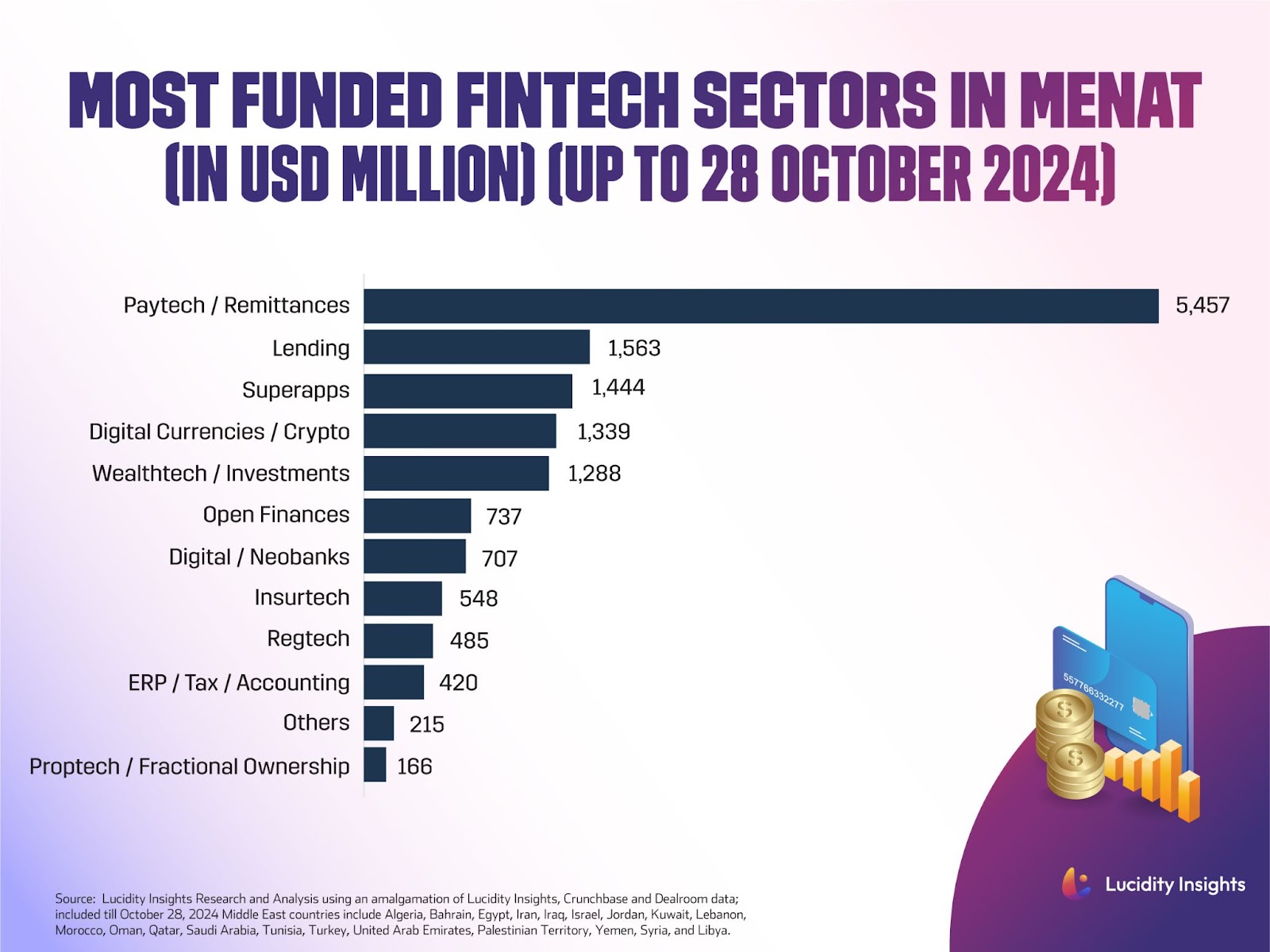

As in most parts of the world, paytech—startups specializing in payments and remittances—has and continues to lead the way, attracting over US $5.4 billion in funding over the past two decades. However, the region is now seeing rapid growth in other fintech verticals, including:

- Lending: Companies like Tabby and Tamara are reshaping consumer finance through innovative credit models like Buy-Now-Pay-Later (BNPL) offerings.

- Superapps: Multifunctional platforms are gaining traction, combining payments, wealth management, and e-commerce.

- Crypto and WealthTech: Startups like Sarwa are catering to a younger, tech-savvy population, democratizing investment and crypto adoption.

This diversification reflects the ecosystem’s maturity, with startups moving beyond payments to address more complex financial needs.

What Lies Ahead?

The Middle East’s fintech sector is entering a pivotal phase, with 2025 set to be a defining year for the region. Key trends such as AI-driven financial solutions, open banking, and embedded finance are poised to reshape the financial landscape, unlocking new opportunities for both startups and investors.

AI will continue to drive hyper-personalized financial solutions, enabling fintechs to anticipate customer needs, streamline compliance workflows, and deliver faster, smarter services. At the same time, open banking frameworks in Saudi Arabia and the UAE will foster greater financial interoperability, empowering startups to integrate seamlessly with traditional banks and innovate at scale.

Emerging verticals such as trade finance, wealthtech, and insurance are expected to become hotbeds of fintech-driven innovation. These sectors, historically underserved in the region, now offer immense potential for startups to tackle inefficiencies, enhance accessibility, and drive economic growth.

As Said Murad, Senior Partner at Global Ventures, puts it, “With a dynamic population and supportive regulatory environments, the Middle East promises to become a hub for fintech innovation, mirroring successes in markets like China, India, and Brazil.”

Additionally, the region’s second-generation founders—entrepreneurs building companies based on pain points they experienced firsthand—are bringing deeper insights and global expertise to the table. Their ventures are positioning the Middle East not just as a participant in the global fintech revolution but as an active shaper of its future.

As Rabih Khoury, Managing Partner at MEVP, emphasizes, “2025 will be the year of fintech.” The convergence of technological innovation, regulatory support, and entrepreneurial talent ensures that the Middle East is well-equipped to tackle its most pressing financial challenges while setting a benchmark for Fintech ecosystems worldwide.

Explore the transformative trends shaping the Middle East’s fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now at Lucidity Insights.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

New Vision, New Goals: Oweis Zahran, Managing Director, OWS Capital

Oweis Zahran is in a reflective mood. “I guess I’ve always been a relatively young entrepreneur, but you know, it was 15 years into doing business when I learned that you only get rich when you sell a company. But you have to build the company first. So, you have to be poor for a really long time before you can get rich,” he says. It’s fair to say the “poor” days are in the past. Now an accomplished global business leader with a track record of identifying opportunities, his biggest success is OWS Automotive.

Today, it is a leading global provider of automotive services. From first response to parts manufacturing and fleet repair, it has become a go-to company for both governments and corporate fleets. And with revenues of US$800 million, 3,000 employees and a footprint in 14 countries,it is – in his own words – “a monster.” If that wasn’t enough, in 2020, he launched OWS Capital, aiming to create unique experiences and cutting-edge businesses in fitness and entertainment verticals. Under the umbrella of OWS Capital, he’s partnered with Holly- wood icon Steve Harvey to establish MELT Holdings and launched Platform Health Club, a state-of-the- art health and wellness gym brand. Other A-listers such as Ryan Reynolds and Jason Momoa have also come on board for different projects. Although it accounts for just 20% of the “Zahran empire”, OWS Capital has a knack of making global headlines for the quality of stars and events it hosts.

In simple terms, is it fair to say that OWS Capital makes sure Oweis Zahran can walk into any restaurant in the world and get the best table – but the bill is paid by…OWS Automotive? “That’s definitely the ideal way to say it. Spot on. Spot on,” he says.

Related: The 100: Oweis Zahran, Managing Director, OWS Capital

Thankfully, his automotive business has been on a roll, experiencing nothing short of exponential growth. Much of the increase in revenues is down to selling his stakes in joint ventures that he has set up over the past decade. And the list of clients Zahran has worked with is nothing short of spectacular: the governments of Brunei, Dubai, and Abu Dhabi stand out, as well as Mobil 1. Plus, Tawazun, an independent UAE government entity that works closely with the Ministry of Defense, Abu Dhabi Police, and security agencies in the UAE.

“We would enter at the highest level, formulate a joint venture or a partnership between one of our companies, whether it’s OWS Automotive or, you know, another one, but we would formulate a partnership between our company and the local government. And then that entity would be the one to provide the service back to the country that it operates in. And it would be a 50% owned by local government or a local authority and 50% owned by OWS or an OWS company,” he says, adding: “That then becomes a company on its own, and sometimes we’ve had situations where, believe it or not, our subsidiary has become bigger than the mother company.”

Some of these have been nothing short of a staggering success, creating thousands of jobs and entities worth several hundreds of millions of dollars. “We’ve gotten to a point where we’re selling a subsidiary every year on average. That’s what gets the revenue so high,” he says.

Zahran points out that almost every cab you see on the roads of Dubai is his customer. And so are 99% of the buses – given a long standing partnership with the RTA. Like all clients, they love not just the range of services but the quality – OWS Automotive’s smallest workshop is 200,000 square feet. The partnership with Steve Harvey has been a mega success; with the two of them teaming up in the formation of Melt Holdings where they have successfully created and delivered some of the region’s largest festivals including the Open Fire Food Festival, Fuelfest Arabia, and the MELT Golf Classic, an annual celebrity golf tournament. The two partners have also expanded into several other sectors, including education, health and wellness, energy, and real estate.

As for Zahran himself, it has been quite a journey – but the key, he says, in everything he does, is not only identifying the right opportunity, but the right team. And he says that more important than who he hires is who he fires. “I would hire someone who’s a superstar, and two years in, three years in, five years in, either they lose passion or lose motivation. Maybe it’s both, and they’re no longer a superstar. They’re no longer the superstar you hired. Well, if that person is number two or de facto number one, in the organization and they’re no longer passionate, you’re in a lot of trouble because what you now have is a spiraling effect in the opposite direction. You shoot yourself in the foot,” he says, adding: “Who you fire to me is a lot more important than who you hire.” As for Zahran himself, how long he actually stays at the helm is also on his mind. He says the travelling has become exhausting, but at least now he is making good money. He explains: “I realized about five years ago that when you have a big company on paper, you don’t have any money in the bank, right? You know, like I looked at a valuation that said my company was worth all these hundreds of millions. But then I looked at my bank account and there was maybe US$300,000 in it and I said, ‘Okay, well, something isn’t making sense here.'”

Source: BNC Publishing

The valuation right now is closer to the billion-dollar mark – and Zahran isn’t shy to admit that at some stage, he will get out. He has been building an impressive real estate portfolio on the side, which is generating considerable passive income. He says: “I don’t want to keep doing this. I mean, I travel literally four times a week, five times a week sometimes. I am building the company horizontally and growing exponentially. This business morphed into a giant in comparison to what it was. I I’m doing that so that I can get a really good valuation. I would like no less than a billion dollars. So, that’s kind of my number and I think it’s also a little bit of a personal thing as well. I always wanted to be able to say I made a billion dollars.”

But what would Oweis Zahran version 2 look like? Surely, he doesn’t want to just sit on a beach and count his money? “I would love to be able to slow down and really focus on what truly makes one happy. And I think that’s giving back,” he says. Zahran recounts a recent incident when he was in Morocco dining at a lavish restaurant. On the way out, he was carrying some left-over food, which he ended up giving to a homeless person he spotted on the street. “He told me this is going to be my breakfast, lunch and dinner for the next 48 hours. So, if you ask me what the future looks like for me, I want to be able to experience the feeling I got from giving that guy that food. I haven’t felt that way in in a long time. I want to do good things.”

Zahran is still only 35 years old but is widely recognized in the business world as one of the “good guys.” Whether it’s through OWS Automotive, OWS Capital – or handing out food on the streets of Marrakesh – you get the feeling he will be doing good things for many years to come.

Related: Influence For Impact: Steve Harvey And Oweis Zahran, Co-Founders, MELT Middle East

The Rise of NeoBanks in the Middle East

Neobanks, digital-only banking platforms without physical branches, are reshaping the global banking landscape. With the neobanking market expected to soar to US $3.3 trillion by 2032, growing at an annual rate of 47.3%, these platforms are catering to today’s fast-paced, tech-savvy consumers by offering 24/7 seamless banking at reduced costs.

Why Neobanks Work

The appeal of neobanks lies in their customer-centricity and lean operating models. By cutting the overhead costs of branches and staff, these digital banks funnel resources into tech innovations, enabling lower fees, faster services, and broader market reach.

Moreover, as trust in traditional banks waned post-2008 financial crisis and events like the 2023 Silicon Valley Bank collapse, neobanks emerged as a simpler, more transparent alternative. The COVID-19 pandemic further accelerated their growth, with widespread smartphone adoption and a shift to digital lifestyles.

The Global Picture

In 2024, the global neobanking market reached US $198 billion, with Europe leading at 38% market share. Two standout examples are Brazil’s Nubank, valued at US $56.4 billion, and the UK’s Revolut, valued at US $45 billion. Revolut has raised US $2 billion, serves 45 million customers globally, and achieved unicorn status in just three years. Its competitor Monzo, with 8.5 million customers, is valued at US $5.9 billion. Revolut and Monzo showcase how neobanks can leverage significant funding to fuel innovation and expansion while maintaining strong valuations as they continue to redefine the banking sector. NuBank is a special case of a neobank that has managed to grow very quickly to reach profitability with a successful IPO under its belt.

NeoBanks in the Middle East

Despite their success, neobanks complement rather than replace traditional banks. Many neobanks operate under licenses from conventional banks or emerge as their spinouts, particularly in regions like the Middle East.

While Europe leads the way in neobanking adoption, the Middle East is emerging as a promising region with unique market dynamics and key players shaping the landscape. Like the rest of the world, the digital banking sector in the Middle East has seen fast growth rates, with some reports indicating a 52% increase between 2021 and mid-2023. As suggested earlier, unlike what you find in the UK, where neobanks are typically independent entities – in the Middle East and Africa region, traditional banks have taken the lead in establishing many of the prominent neobanks in the market themselves.

Fintech adoption across the GCC markets in particular is quite high, due to its young, digitally savvy population and supportive regulatory environments. Countries like the UAE and Saudi Arabia lead the way by issuing licenses to digital-only banks like Zand, Wio and D360 Bank. In the UAE, one of the leading neobank markets in the Middle East, a 2022 survey by Finder revealed that one in five adults had a neobank account. Over 40% of the country’s banking population is projected to have a neobank account by 2027.

Neobanks are increasingly coming online with customized financial products and services to cater to specific niche customer segments. The unbanked or low-income, mobile-first customer is one such segment, where products such as microloans, instant mobile payments and remittances are offered. This trend of identifying distinct consumer groups and building out a bank specifically to meet their needs is likely to continue.

Neobanks are not just a trend—they’re a transformative force redefining how banking is done. In the Middle East, where innovation meets tradition, these digital-first platforms are carving out a significant space in the financial sector, addressing the unique needs of diverse customer segments. As they continue to evolve, collaborate, and innovate, neobanks are poised to complement traditional banks, providing consumers with more accessible, tailored, and convenient financial solutions. The future of banking is digital, and the Middle East is firmly on the path to becoming a global hub for this revolution.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

Why Startups Are Investing in ERP Systems Earlier than Ever

For years, Enterprise Resource Planning (ERP) systems were viewed as expensive tools only available to large, established corporations with complex operations. Startups, by contrast, couldn’t possibly afford, let alone lean into such centralized tools to manage their processes. But times are changing. Today, we are seeing more and more startups, especially from the Fintech space, investing in cloud-based, modular and agile ERP systems at younger stages of the business, reshaping how they operate, scale, and compete.

What’s driving this shift? A convergence of factors unique to today’s business environment. The rise of cloud-based ERP has significantly lowered adoption barriers, providing scalable solutions at low cost, implementable even for the smallest of ventures. The COVID-19 pandemic further accelerated this trend, pushing companies worldwide to embrace flexible working arrangements and adopt systems capable of supporting distributed teams in real-time.

Simultaneously, the growing complexity of regulatory requirements – especially within the Fintech space – and the increasing reliance on data-driven decision-making have made earlier ERP adoption not just beneficial but essential.

The Cloud ERP Revolution

In the past, ERP systems were synonymous with hefty on-premise setups—expensive, resource-intensive, and out of reach for most small and medium enterprises (SMEs). However, the emergence of cloud-based ERP has transformed this narrative, offering a flexible and cost-effective alternative. Cloud ERP solutions are enabling SMEs to adopt these systems earlier than ever.

Between 2018 and 2024, the market for cloud ERP nearly doubled, achieving a CAGR of 12.96%—outpacing the growth of its on-premise counterpart. This momentum is to accelerate over the next 5 years; cloud ERP is forecasted to grow at 15.03% annually through 2030, surpassing US $47 billion by the end of the decade. While on-premise ERP will continue to expand, its growth is expected to moderate, highlighting a paradigm shift.

This shift isn’t just about technology; it’s about meeting the modern demands of agility, scalability, and accessibility. The SME segment is expected to record the highest CAGR during the forecast period. Unlike their larger counterparts, SMEs benefit more from The modular and adaptable nature of cloud ERP, which allows them to implement only the features they need. Market data consistently shows that SMEs are driving demand for cloud ERP, drawn by its ability to streamline operations without overburdening budgets.

For startups, the benefits are clear:

• Lower upfront costs: Subscription-based pricing eliminates the need for significant capital expenditures, making ERP accessible even to cash-strapped ventures.

• Ease of deployment: Cloud ERP systems are faster to implement, allowing startups to focus on their core operations without lengthy disruptions especially as startups are crippled by legacy IT infrastructure.

• Scalability and flexibility: As startups grow, cloud ERP systems can scale seamlessly, accommodating new users, locations, and business functions.

Beyond the operational efficiencies and process improvements that ERP systems traditionally deliver—such as streamlined workflows, enhanced resource management, and centralized data control—cloud ERP is unlocking entirely new opportunities for startups. By removing the limitations of on-premise infrastructure, these systems are not only more accessible but also more aligned with the demands of modern business environments. For startups, this shift is about more than cost savings; it’s about agility, adaptability, and positioning themselves for future growth.

Adapting to the new normal of remote and hybrid Work

The COVID-19 pandemic didn’t just accelerate the adoption of remote work—it redefined the workplace. What started as a necessity during lockdowns has now evolved into a permanent shift, with hybrid and remote work becoming a growing standard for businesses globally.

More startups have embraced hybrid and remote work models as a natural extension of their flexibility and lean operational structures. Unlike larger corporations with established physical offices and legacy more rigid systems, startups often prioritize agility and adaptability, making remote or hybrid setups a strategic choice. This approach enables them to attract top talent, optimize costs, and remain competitive in fast-changing markets.

As startups grow, managing distributed teams and ensuring operational cohesion becomes increasingly complex. Cloud-based and increasingly innovating ERP systems are proving invaluable in addressing these challenges, particularly in facilitating virtual HR processes and enhancing employee engagement within distributed work environments. These systems enable seamless operations by providing employees with the tools and resources needed to work efficiently from anywhere with an internet connection. Their accessibility and adaptability make cloud ERP an essential component for startups navigating the demands of remote and hybrid work.

Consider the example of Remote, a startup that specializes in enabling companies to hire talent from anywhere. By implementing SAP’s cloud ERP system, Remote was able to manage its operations effectively while experiencing rapid growth, expanding to 55 countries and over 650 employees in just two years. The platform provided the structure and visibility necessary to support its hybrid workforce while ensuring efficiency and compliance. As Pedro Monteiro de Barros, VP of Finance at Remote, noted, “Working with a company like SAP allows Remote to scale its operations efficiently and cost-effectively.”

Navigating the increasing complexity of regulatory compliance

Globally, companies are grappling with a rapidly evolving landscape of regulatory requirements. From stringent data privacy laws such as GDPR to global anti-money laundering (AML) standards, the compliance burden has reached unprecedented levels. These regulations demand meticulous tracking, precise reporting, and a structured approach to managing sensitive information—tasks that can easily overwhelm startups relying on fragmented tools or manual processes. This not only strains their resources but also diverts attention from critical priorities such as scaling operations and driving innovation.

ERP systems provide startups with a much-needed solution by centralizing data and automating compliance workflows. These systems simplify reporting, ensuring accuracy and timeliness, while built-in safeguards and audit trails enhance data integrity and reduce the risk of non-compliance. Moreover, for startups operating across multiple jurisdictions, ERP systems standardize processes to meet diverse regulatory demands, enabling them to navigate cross-border complexities with greater ease.

A perfect example of this is LetsGetChecked. As a medical technology company committed to bringing healthcare into the home, it operates within a highly regulated environment. This includes adhering to stringent regulations like the European Union’s General Data Protection Regulation (GDPR) and the U.S. Health Insurance Portability and Accountability Act (HIPAA), which govern the management of sensitive patient data and medical records.

With rapid operational growth, LetsGetChecked’s legacy finance and business management systems struggled to meet the company’s evolving demands. Recognizing the need for a robust digital foundation, the company implemented SAP’s ERP solution to support its expansion while ensuring compliance with complex regulatory requirements. The platform’s integrated features provided the scalability and precision needed to align with strict regulations, enabling LetsGetChecked to maintain its commitment to regulatory excellence while continuing to grow.

Empowering Data-Driven Decision-Making

Data has emerged as a critical strategic asset. However, raw data is only valuable if it can be effectively harnessed, analyzed, and acted upon. ERP systems play a pivotal role in this transformation by consolidating data from across the organization into a unified platform, breaking down silos and enabling comprehensive analysis.

Modern ERP systems are far more than simple data repositories; they are sophisticated tools that integrate advanced technologies like artificial intelligence (AI) and predictive analytics to transform raw data into actionable insights. For startups, these capabilities are game-changing. By analyzing both historical and real-time data, ERP systems allow companies to anticipate trends, forecast market shifts, and better understand customer behavior. Predictive analytics further enable startups to optimize operations by streamlining resource planning, improving demand forecasting, and even implementing proactive maintenance strategies to avoid costly disruptions. Additionally, AI-powered dashboards provide decision-makers with real-time metrics, empowering them to make faster, more informed choices that drive growth and operational efficiency.

Supporting Fundraising and IPO Preparations

For startups, access to capital is a critical driver of growth, whether it involves securing venture capital during early funding rounds or preparing for an Initial Public Offering (IPO) or an acquisition. In this competitive landscape, financial transparency and operational clarity are no longer optional—they are prerequisites. Investors and regulators alike demand a level of organizational maturity that instills confidence in a startup’s ability to scale and deliver on its promises.

A well-implemented ERP system is a clear signal of a startup’s preparedness. It demonstrates not only operational control but also the capacity to scale without encountering bottlenecks or inefficiencies. Nowhere is this more evident than during the due diligence process—a critical stage in fundraising. Startups are required to present comprehensive data rooms containing financial statements, operational metrics, and compliance documentation. For those relying on disjointed or manual systems, assembling this information can be a time-consuming and error-prone task. ERP systems streamline the process by centralizing critical data, ensuring that the information presented is accurate, consistent, and easily accessible to potential investors. This efficiency significantly reduces the time and effort involved, providing startups with a leg up during the process.

The importance of investor-ready data rooms is a sentiment echoed by venture capitalists. Sonia Weymuller, co-founder and general partner of VentureSouq, highlighted this in an episode of The Perfect Pitch podcast series by Lucidity Insights: “Just like you’re building your product to make it as user-friendly as possible, make your data rooms as investor-friendly as possible.” ERP systems can help in this way, by offering startups the tools they need to present their operations with clarity and professionalism, meeting the high expectations of today’s institutional investors.

When preparing for an IPO, the stakes are even higher. Going public requires meticulous adherence to regulatory standards, from compiling accurate financial disclosures to maintaining real-time operational transparency. ERP systems streamline these efforts by automating compliance workflows and consolidating financial and operational data into a unified system. This not only facilitates public reporting but also enhances credibility, showing regulators and investors alike that the startup operates with the rigor of a mature enterprise. In case of an acquisition, according to Rabih Khoury, Managing Partner & Chief Exit Officer at Middle East Venture Partners (MEVP) “ERP systems create more value to an acquiror by clearly highlighting the value of the target’s data”. ERP system providers have been maturing and helping to unleash the value of Big Data and Machine Learning especially with the advent and accessibility of AI.

The case for early ERP adoption is clear. For founders, the message is simple: don’t wait until inefficiencies or missed opportunities force a transformation. Investing in a scalable, cloud-based ERP system today is an investment in your startup’s resilience, credibility, and capacity to grow tomorrow. The tools are there, the benefits are proven, and the future rewards are limitless.

Learn more about how SAP supports scale-ups in their growth journey by visiting this link.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

The Path to Sustainable Fintech Growth in MENA: SAP’s Perspective

Transition to Sustainable Growth in the Fintech Sector

The Fintech sector is transitioning from a period of explosive growth to one that emphasizes sustainable and profitable development. Over the last decade, advancements in technology have propelled Fintech to become a leading sector within financial services, fueled by rapid digitization and shifting consumer preferences. However, a market correction that began in 2022 has tempered this fast-paced expansion, leading to a decrease in both funding and deal activity as economic uncertainties linger.

Growth of MENA Fintech Landscape

At the same time, the MENA Fintech landscape has expanded dramatically, with a surge in startups and innovative financial services. The region is home to hundreds of Fintech companies, addressing a variety of sectors, including payments, lending, insurance, and wealth management. This growth is fueled by a young, tech-savvy population eager for modern financial solutions.

Venture Capital investment in regional Fintech startups have seen significant increases, with funding reaching record levels in recent years. This influx of capital is vital for scaling operations and expanding product offerings. While this is very promising for the flourishing of the MENA Fintech sector, it also brings about a fierce competition for investment, for talent and for customer acquisition among Fintech players.

Challenges in Raising Capital

Recent studies indicate that there are just as many Fintech startups in MENA that are unfunded, as there are funded startups; making it harder to raise capital for a regional Fintech, than it is to raise capital for a regional AI, healthtech or foodtech startup.

Therefore, not only will it be important to address a specific niche with a strong value proposition, but Fintech startups will need to prove operational efficiency, high scalability to support hypergrowth, all while keeping a close eye on profitability and by total cost of ownership (‘TCO’). They must check the mark on the most important key performance indicators (‘KPIs’) to be able to stand out from the crowd in the eyes of the investors. This is easier said than done.

To attract funding and become the next unicorn, a unified data platform strategy will be critical. From customer to operational data, from HR to finance data, Fintechs need to have a holistic view of their data to be able to surface game-changing insights that will help them steer their company in the right direction and grow profitably.

SAP: Supporting Fintech Growth

At SAP, we are proud to be one of the few software vendors that can address the end-to-end value chain needs of a Fintech from infancy to global Fintech unicorn. With SAP S/4HANA Cloud as the clean core Cloud ERP and back-bone for all other enterprise applications, SAP provides Fintech specific innovations, and modular design offering line-of-business solutions like HR, CRM and procurement, all residing on one common, unified Business Technology Platform, powered by SAP Business AI.

According to 2024 survey results shared by the Wall Street Journal, “Tech leaders are finally giving priority to the modernization of their ERP systems. ERP applications are the second-most likely to move to the cloud in the next two years, followed by databases.”

Future Focus on Data Analytics and AI

As Fintech companies continue to align their business strategy with their technology strategy, there will be an increased focus on data analytics, unleashing the power of AI and on having seamless, natively connected systems across the enterprise to realize value. This is the reason why global market leaders like PayPal and Monzo have chosen SAP, and we’re excited to see Fintech’s in the Middle East use our solutions to help scale their businesses beyond what they thought was possible.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

The Barriers to Fintech and Its Adoption in the Middle East

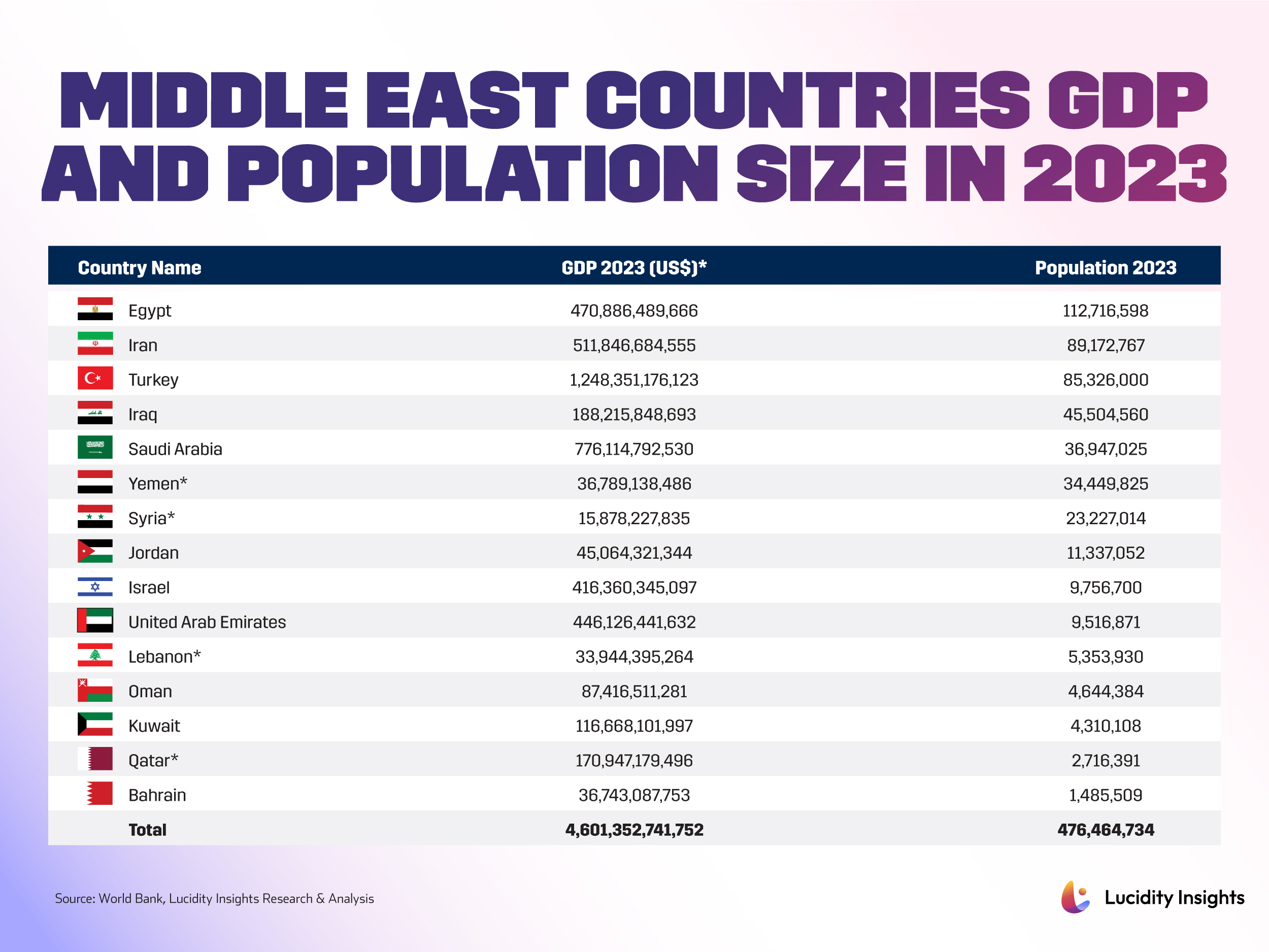

With a population nearing 500 million and projected to exceed 700 million by 2050, the Middle East holds immense potential as a Fintech hub. However, despite the region’s key markets—such as Saudi Arabia, the UAE, Egypt, Turkey, and Iran—ranking among the world’s top 50 economies by GDP, significant barriers remain.

Regulatory fragmentation hampers cross-border collaboration, while a shortage of skilled tech talent stifles innovation. Limited access to early-stage capital further constrains startup growth. These challenges persist even as high mobile and internet penetration, strong remittance flows, and government-led initiatives lay the groundwork for rapid Fintech adoption. Addressing these obstacles is crucial to unlocking the full potential of the Middle East’s Fintech landscape.

1. Regulatory Fragmentation

One of the most significant barriers facing Fintech in the Middle East is the fragmented regulatory environment, which complicates cross-border expansion for companies across the region. Each country maintains distinct regulatory frameworks, making it difficult for Fintech companies to offer uniform services across multiple markets. This lack of harmonization leads to costly and time-consuming processes, with many Fintech startups reporting that navigating cross-border regulatory approvals can take over a year.

To illustrate the impact, consider a Fintech firm aiming to access the 9.5 million people in the UAE or the nearly 37 million people in Saudi Arabia. Despite both being members of the GCC, a Fintech licensed in Saudi Arabia would still need to undergo a separate licensing process in the UAE to reach that consumer base. For smaller markets like Qatar and Bahrain, this repeated licensing requirement further strains smaller Fintech firms, which often lack the financial resources to register in multiple jurisdictions. For instance, in markets like Kuwait (4.3 million people) or Oman (4.6 million people), the process of regulatory compliance may outweigh the potential market benefits for newer entrants.

A streamlined approach, like Europe’s “passporting” model, could significantly boost Fintech’s growth across the region by enabling companies to operate freely across multiple GCC countries. Although the Digital Cooperation Organization, founded by countries such as Saudi Arabia, Bahrain, and Jordan, aims to improve regional digital integration, more concrete regulatory alignment is necessary to facilitate Fintech expansion and competition.

The fragmented landscape not only poses a challenge to Fintech startups but also limits the total addressable market (TAM) for digital financial services in each country, slowing down the region’s overall Fintech adoption and innovation potential.

2. Talent Shortage

Another challenge is the significant talent shortage, particularly in advanced technical roles. While the sector is expanding rapidly, the region lacks a sufficient supply of specialized professionals in critical areas like cloud computing, APIs, blockchain, and cybersecurity. This gap is particularly acute in GCC countries like Saudi Arabia, Qatar, and Kuwait, where 75% of employees in Kuwait and 60% in Qatar report a lack of specialized skills. The region is making some strides, with Saudi Arabia and the UAE investing in large-scale educational programs to address the shortage. Saudi Arabia’s US $1.2 billion initiative, aimed at improving digital skills for 100,000 youth by 2030, and the UAE’s National Program for Coders, offering Golden Visas to skilled professionals, reflect efforts to address this talent gap.

However, competition for tech talent is fierce, driving up costs for recruiting skilled engineers and programmers. Firms in the Middle East are now paying more to attract talent than in established tech hubs like London or Singapore, making it difficult for startups to compete. Only 6% of the GCC workforce is employed in technology-related jobs, far below what is needed to support the sector’s growth, leaving firms struggling to find qualified candidates locally.

Government-mandated localization policies, particularly in Saudi Arabia, add another layer of pressure, as firms are tasked with training domestic talent to assume leadership roles. This places additional strain on businesses, which must balance local hiring requirements with the urgent need for expertise.

Lastly, the low representation of women in leadership roles within Fintech remains a challenge, as only 9% of MENA startups have a woman on their executive team, far below global benchmarks. This gender imbalance poses a challenge, as global studies link gender-diverse leadership teams with higher profitability and better innovation outcomes.

3. Limited Access to Capital

Fintech startups in the Middle East also have significant challenges due to limited access to capital hindering their growth and scalability. Despite the economic prosperity in the GCC, VC investment remains small. Saudi Arabia holds only 0.08% of global VC funding, far below its 0.9% share of global GDP. This disparity highlights a lack of sufficient private investment compared to other global financial hubs.

According to a report by Strategy&, sovereign wealth funds (SWFs) like the UAE’s Mubadala and Saudi Arabia’s Public Investment Fund (PIF) are the primary drivers of Fintech funding in the region. However, this reliance on public funding leaves gaps, particularly in early-stage investment, where private venture capital is essential for fostering innovation and growth. While efforts such as the Middle East Venture Capital Association, launched in 2018, aim to address these challenges, progress has been slow, and many Fintech startups struggle to secure the early capital needed to scale. While there have been increases in funding, the depth of the investment pool remains shallow, particularly in comparison to mature Fintech ecosystems in Europe or North America.

One of the other challenges limiting investor appetite is the lack of exit options. Middle Eastern IPO and M&A markets remain underdeveloped in comparison to other major markets, which discourages investment, especially in early-stage ventures. Investors often have limited pathways to liquidate their holdings, hindering the recycling of capital back into the ecosystem.

In conclusion, the Middle East Fintech sector requires greater private-sector participation, deeper early-stage investment pools, and more developed capital markets to support its growing innovation landscape. Without addressing these barriers, Fintechs in the region will struggle to scale and achieve their potential in the global financial ecosystem.

4. Infrastructure Gaps and Financial Exclusion

Despite impressive mobile and internet penetration rates in the GCC countries, parts of the Middle East face significant infrastructure challenges that hinder Fintech adoption. Countries like Lebanon, Syria, and Yemen continue to struggle with unreliable internet connections, frequent power outages, and an overall underdeveloped digital ecosystem. These limitations create barriers to financial inclusion, especially in rural areas where access to digital services is crucial but unavailable.

Moreover, a crucial infrastructure gap in the region is the lack of robust credit bureau systems, which are vital for assessing creditworthiness. Credit coverage in many Middle Eastern countries is inadequate, with private credit bureaus covering just over 20% of adults across the broader region. While Israel and several GCC countries have relatively high credit bureau coverage (with some surpassing 50- 60%), other nations like Lebanon and Jordan lag significantly behind. This gap makes it challenging for financial institutions to evaluate potential borrowers, particularly small and medium-sized enterprises (SMEs), and restricts access to credit for individuals and businesses alike.

For individuals, this lack of infrastructure exacerbates financial exclusion. Countries like Egypt, where nearly two-thirds of the population remains unbanked, illustrate the difficulty of reaching rural or underserved communities. Similarly, the high number of unbanked individuals in Lebanon, Palestine, and Jordan highlights the need for better financial infrastructure and systems, such as mobile banking and Fintech solutions, that can address these challenges.

SMEs face even greater barriers. Although they play a vital role in the economies of countries like Saudi Arabia and Egypt, SMEs often lack access to formal credit systems, relying instead on informal or costly financing options. The absence of comprehensive credit bureaus compounds these difficulties, limiting their ability to secure loans and expand operations. In Saudi Arabia, for instance, SMEs receive only about 2% of total bank lending, one of the lowest rates globally, highlighting the urgent need for improved infrastructure to assess and serve smaller businesses.

While Fintech offers promising solutions to these challenges, infrastructure gaps in broadband access, credit data, and digital systems need to be addressed to unlock the full potential of financial inclusion in the Middle East. Without these critical upgrades, the region risks leaving large portions of the population and business community underserved, unable to participate fully in the financial system.

5. Data Sovereignty and Localization Laws

Data sovereignty laws requiring that data be stored locally add another layer of complexity for Fintech firms seeking to scale. Countries like Saudi Arabia and the UAE have stringent regulations on data localization, which can be costly and burdensome for international Fintech companies. These laws can also restrict cross-border data flow, further complicating the scaling of Fintech services across multiple jurisdictions.

Conclusion

The Middle East is a region of immense potential for Fintech growth, driven by its high mobile penetration, government support, and economic diversification efforts. However, challenges such as regulatory fragmentation, talent shortages, limited access to capital, and infrastructure gaps continue to hinder widespread Fintech adoption. Addressing these barriers requires coordinated efforts from governments, the private sector, and international investors. By fostering a more unified regulatory environment and investing in talent and infrastructure, the Middle East can unlock the full potential of its Fintech sector and cement its position as a global Fintech hub.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

Building the Future: Drivers to Fintech and Its Adoption in the Middle East

The Middle East is home to nearly 500 million people, representing about 5.9% of the global population, and is projected to grow to over 700 million by 2050. Despite economic disparities, several countries, including Turkey, Saudi Arabia, Iran, Egypt, and the UAE rank among the top 50 globally by GDP.

This economic strength, coupled with some strong drivers, is creating a fertile ground for Fintech development. As regional governments pursue economic diversification, financial technology is emerging as a key driver for modernization and growth, enabling the Middle East to position itself as a future Fintech hub. Let’s explore what the drivers and barriers are to Fintech adoption and acceleration in the region.

The Drivers of Fintech in the Middle East

1. High Mobile and Internet Penetration

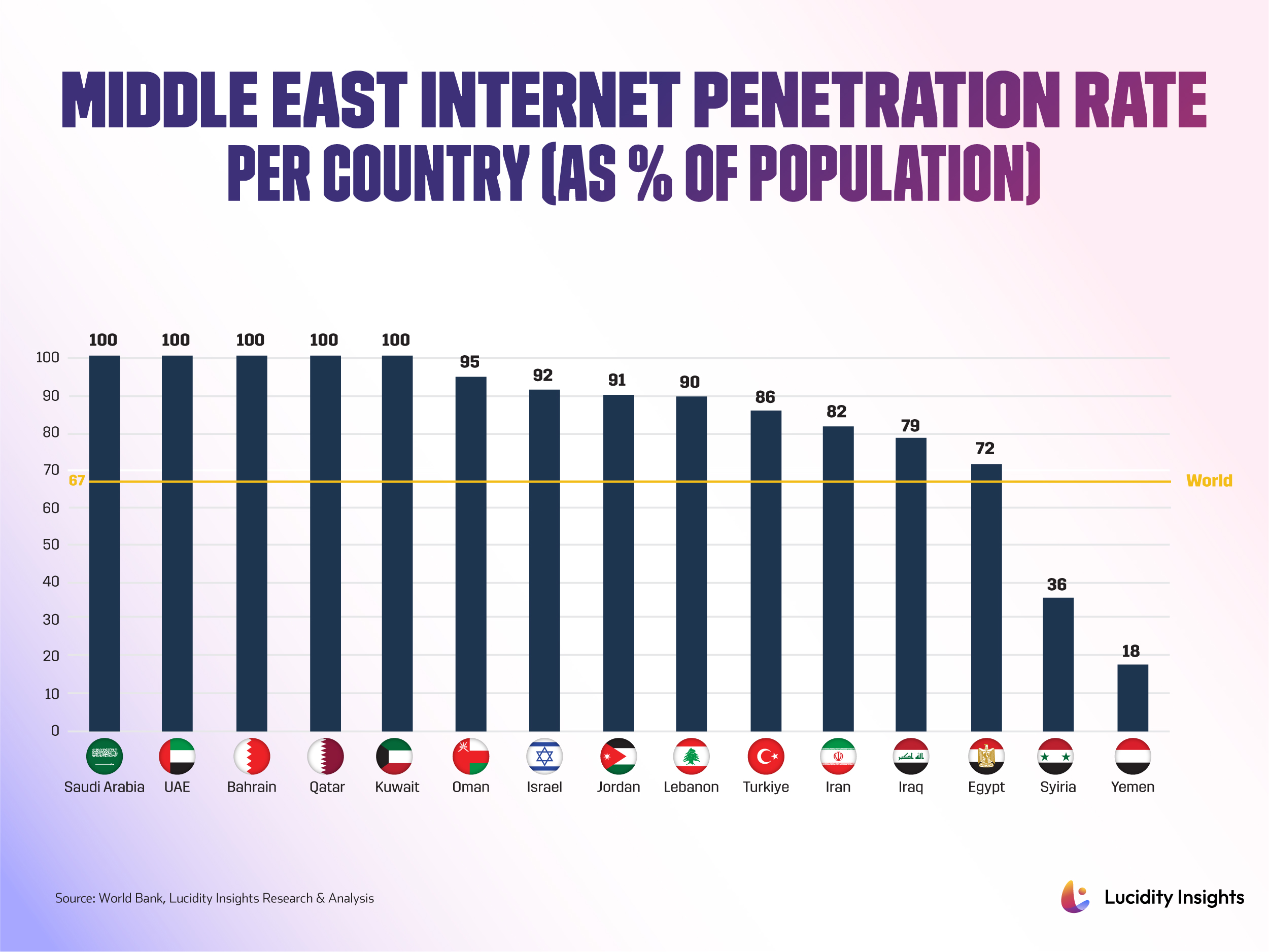

87% of countries in the Middle East have an internet penetration rate superior to the global average with countries like the UAE, Saudi Arabia, Bahrain, Qatar, and Kuwait boasting a 100% penetration rate. Mobile cellular subscriptions as a percentage of the population follows a similar trend with an average above 100% ranging from 58% for Yemen to more than twice the population in the United Arab Emirates. High mobile and internet penetration rates provide a strong foundation for the growth of Fintech, particularly mobile-based financial services such as mobile money and mobile banking.

2. Strong Remittance Markets

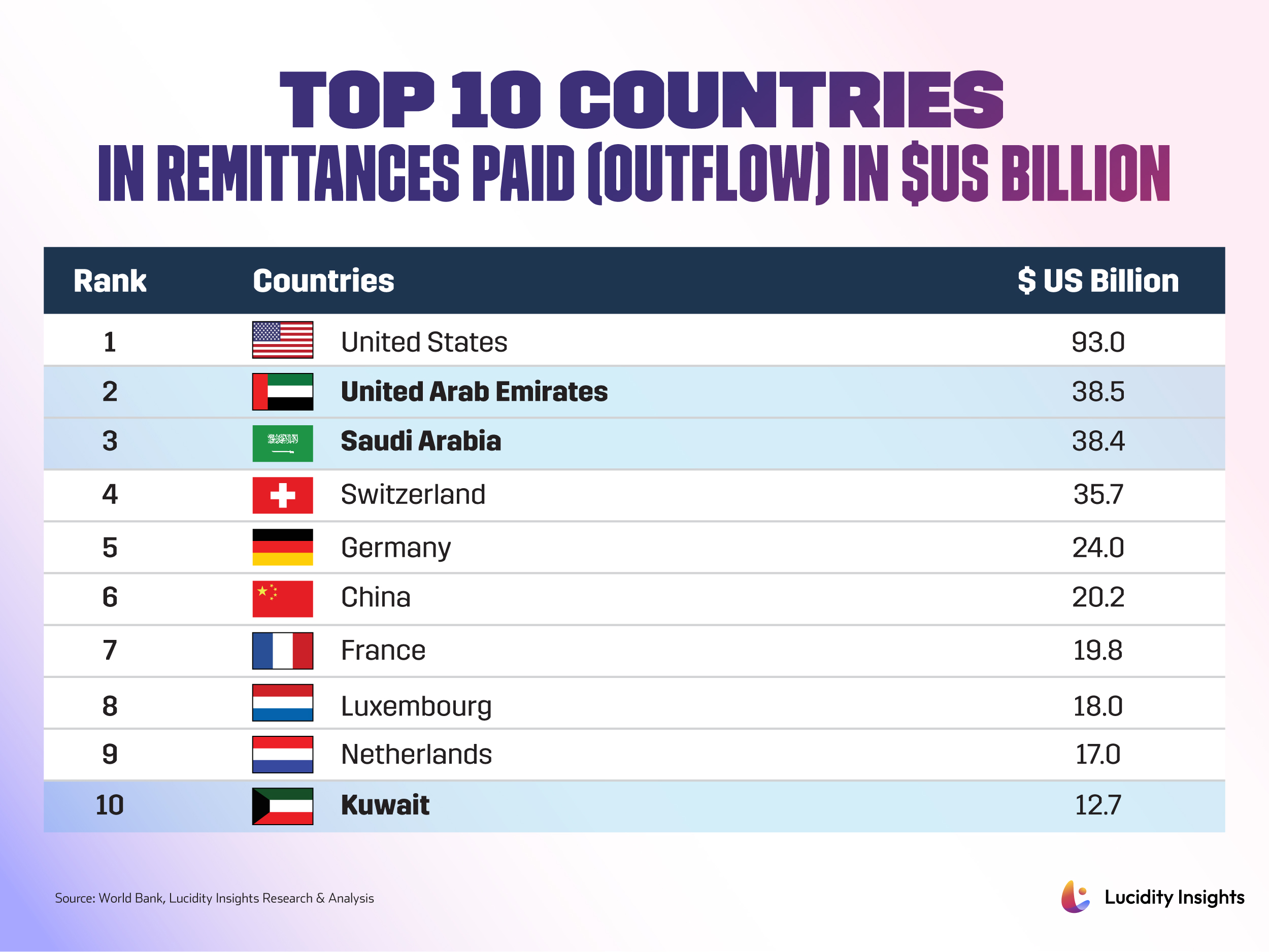

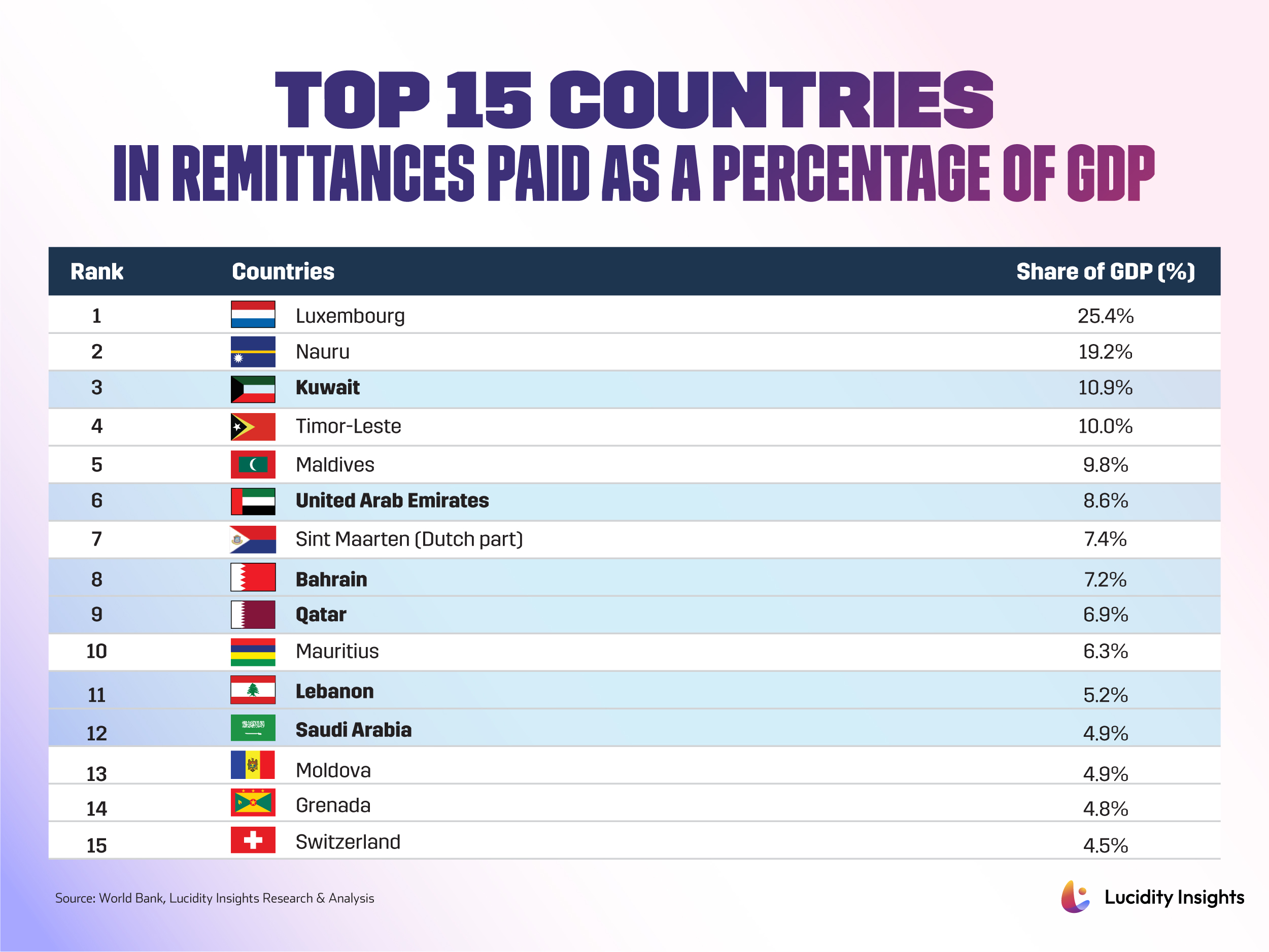

Thanks to significant migration over the past decades, the Middle East is home to some of the world’s largest remittance corridors. Countries like Saudi Arabia, the UAE, and Kuwait are major sources of remittance outflows to South Asia, Africa, and Southeast Asia, consistently ranking in the top 10 globally. Saudi Arabia and the UAE are among the top three, just behind the U.S. Outflows also represent a significant share of GDP, with six Middle Eastern countries in the global top 15, led by Kuwait at 10.87%. Meanwhile, less affluent nations benefit from inflows—Egypt ranks 11th globally by volume, while Palestine and Lebanon rank 14th and 18th by remittances as a percentage of GDP. Fintech innovations such as blockchainbased transfers and mobile platforms are gaining traction by reducing transfer times and costs, further transforming the remittance landscape in the region.

3. Government Initiatives and Supportive Regulation

Governments across the Middle East, particularly within the Gulf Cooperation Council (GCC), have been instrumental in fostering a robust Fintech ecosystem through proactive policies, regulatory sandboxes, and strategic initiatives. Regulatory sandboxes in hubs like Saudi Arabia, the UAE, Qatar, and Bahrain enable Fintech start-ups to test and refine innovations under controlled conditions. Institutions like Fintech Saudi, the Dubai International Financial Centre (DIFC), Abu Dhabi Global Market (ADGM), and Bahrain Fintech Bay are key facilitators, providing frameworks that encourage experimentation and innovation.

Saudi Arabia’s National Fintech Strategy 2030 exemplifies a long-term commitment to becoming a global Fintech leader, targeting 500 active Fintechs by 2030. Similarly, Dubai’s DIFC Innovation Hub and ADGM in Abu Dhabi stand at the forefront of Fintech innovation by supporting open banking, which is designed to integrate Fintech solutions with existing banking systems, spurring competition and creative solutions.

Cross-border collaboration is also slowly being addressed with the example of the Digital Cooperation Organization (DCO). The DCO was formed in 2020 by countries like Saudi Arabia, Bahrain, Jordan, and Qatar, and aims to enhance digital prosperity and accelerates digital economy growth across the region. In 2022, the DCO launched the Startup Passport initiative, simplifying regional market expansion for entrepreneurs and making cross-border operations more seamless and cost-effective. This initiative serves as a powerful catalyst for scaling Fintech ventures and encouraging cross-border financial innovation across the Middle East.

Together, these initiatives not only facilitate a more conducive environment for Fintech growth but also improve access to international markets and stimulate digital innovation across the region. The combination of regulatory support, cross-border collaboration, and progressive Fintech strategies will continue to drive the rapid adoption of financial technologies in the Middle East.

4. Islamic Finance and Takaful (Islamic Insurance)

With more than 90% of the Middle East’s population being Muslim, Islamic finance holds significant cultural and market importance, providing fertile ground for Fintechs offering Shariah-compliant products such as Takaful (Islamic insurance), loans, and investments. Although it remains a small segment of global finance, Islamic finance is one of the fastest-growing sectors. By 2022, assets in the global Islamic finance industry had surged to US $4.5 trillion, with Islamic banking representing 72% of this. Over the past decade, the sector expanded by 163% and is projected to hit US $6.7 trillion by 2027, driven by rising demand for ethical, Shariah-compliant financial services.

This accelerated growth, coupled with the rising sophistication of Fintech solutions targeting the Muslim demographic, positions Islamic finance as a crucial driver for innovation and growth within the region’s financial sector. Fintech platforms, particularly those offering Takaful and digital Islamic banking solutions, are uniquely positioned to capture this rapidly expanding market by leveraging the regulatory frameworks and cultural demands shaping the Middle East.

5. Economic Diversification and Vision Plans

Economic diversification plans across the region are driving Fintech adoption. These initiatives aim to reduce dependence on oil revenues and build a knowledge-based economy, with Fintech often playing a key role in this transformation. Countries are investing heavily in digital infrastructure, talent development, and innovation hubs, making Fintech a cornerstone of their future economies.

For examples, in Saudi Arabia, Vision 2030 positions Fintech as a pivotal sector to help modernize the economy and drive job creation. Through initiatives like Fintech Saudi, the country provides support for startups, nurtures partnerships, and fosters a culture of financial innovation, aligning with the broader goals of Vision 2030 to strengthen Saudi Arabia’s position as a regional tech and finance leader.

Dubai’s D33 Economic Agenda underscores the emirate’s commitment to becoming a top global economic hub by 2033, with Fintech as a critical component. Initiatives such as the Dubai International Financial Centre (DIFC) Innovation Hub and the Dubai Cashless Strategy provide infrastructure and support for Fintech growth, reinforcing Dubai’s role as a nexus for digital finance in the region.

Similarly, Bahrain’s Economic Vision 2030 has seen the development of Bahrain Fintech Bay, a hub dedicated to nurturing the Fintech ecosystem by offering incubation, co-working spaces, and networking opportunities with investors and financial institutions. This initiative aims to position Bahrain as a Fintech innovation center in the Gulf.

In Qatar’s National Vision 2030, Fintech is a cornerstone in creating a diversified, knowledge-driven economy. The Qatar Financial Centre (QFC) and Qatar Fintech Hub by Qatar Development Bank actively supports Fintech ventures by providing a favourable regulatory environment and encouraging innovation and investment in the sector.

Together, these national agendas emphasize the region’s dedication to embedding Fintech as a core driver of economic diversification, signaling its strategic importance in shaping the Middle East’s future economy.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.