SAP Digital Currency Hub: Transforming Cross-Border Payments Through Digital Currencies

For decades, the world of cross-border payments has been ripe for disruption. Businesses, particularly small and medium-sized enterprises (SMEs), have long endured high fees, opaque processes, and sluggish transaction times as they navigate international transactions. These inefficiencies have become glaring pain points in today’s globalized digital economy, where money needs to move as fast as ideas.

The persistent challenges in cross-border payments

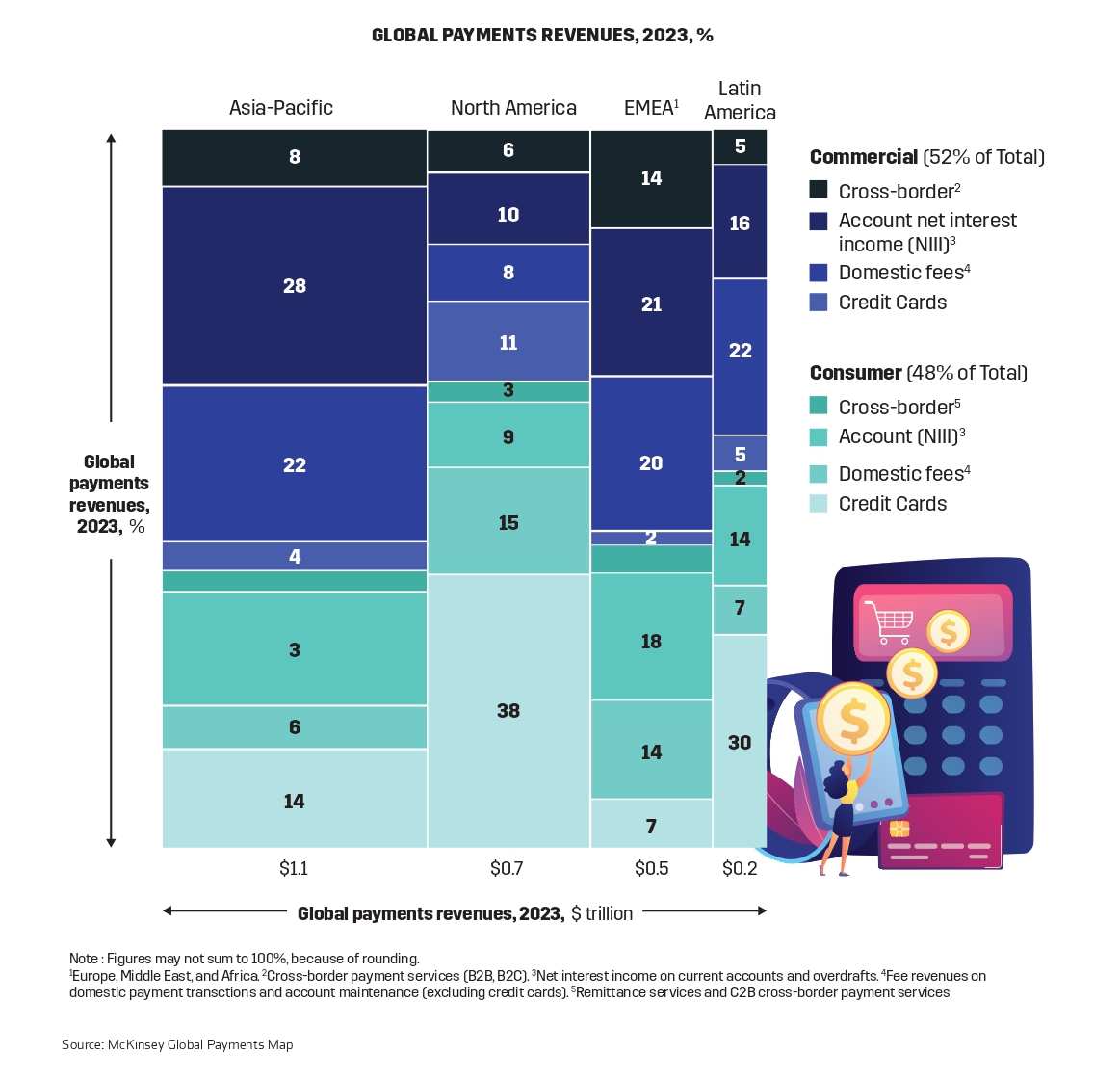

According to McKinsey & Company, the global payments industry processed 3.4 trillion transactions in 2023, representing an astonishing US $1.8 quadrillion in total value.

This activity generated a revenue pool of US $2.4 trillion. Cross-border payments, spanning both consumer and commercial verticals, contributed approximately 12% of these global revenues. Notably, commercial payments dominated this segment, accounting for over 70% of cross-border payment revenues.

The infrastructure supporting crossborder payments was built for a different era and has failed to keep up with the speed, cost-efficiency, and transparency demanded by today’s businesses. Companies face five critical challenges that highlight the inefficiencies of traditional systems:

1. High Costs: Sending $100,000 via wire transfer can cost between $150 and $500. Even card-based transactions, like those processed through Visa or Mastercard, typically incur fees of $100 to $300 (based on CryptoCrunchApp). These costs are especially burdensome for SMEs with limited margins.

2. Availability and Delays: Payments often require several days to process, exacerbated by the lack of 24/7 availability. The involvement of multiple banks, currency conversions, and intermediaries further extends processing times. These delays not only disrupt cash flow but also create significant operational challenges for businesses relying on timely transactions.

3. Security Risks: The involvement of multiple intermediaries increases the risk of fraud and cyberattacks. Each additional party in the payment chain represents a potential vulnerability.

4. Liquidity Constraints: Delayed transactions can tie up valuable working capital, leaving businesses unable to reinvest, pay suppliers, or cover day-to-day expenses in a timely manner.

5. Lack of Transparency: The complexity of cross-border payments often leaves businesses uncertain about the status, costs, or timing of transactions. This lack of clarity makes financial planning and reconciliation more difficult.

These challenges disproportionately affect SMEs and startups, especially those operating in emerging markets. In these regions, fragmented regulatory environments and limited banking infrastructure further exacerbate the inefficiencies.

How blockchain and stablecoins are changing the cross-border payment landscape

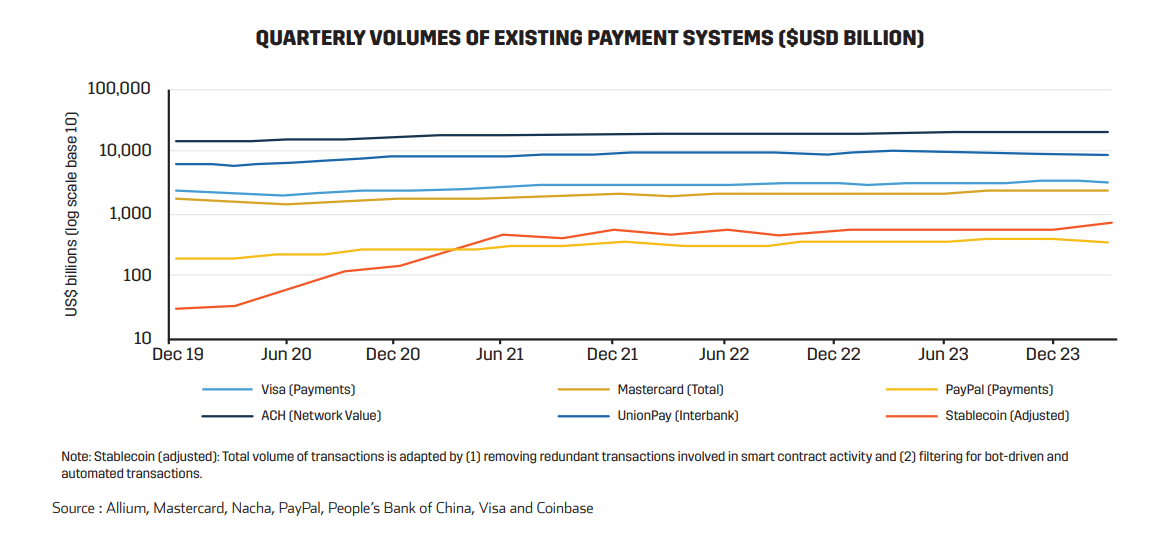

Blockchain technology and stablecoins have emerged as powerful solutions to the inefficiencies of traditional payment systems. By eliminating intermediaries, blockchain enables near-instant settlement and reduces transaction costs dramatically. Networks like Solana and the Bitcoin Lightning Network exemplify the potential: Solana processes payments for a mere $0.00025 per transaction, while the Bitcoin Lightning Network costs less than $0.01 per transfer.

Stablecoins, digital assets pegged to fiat currencies, provide a practical alternative for crossborder transactions by maintaining a stable value. Unlike traditional cryptocurrencies, which are subject to significant price volatility, stablecoins offer predictability, making them particularly useful for payments and remittances. In 2023, stablecoin settlement volumes surpassed US $3.7 trillion globally , reflecting their growing role in the digital economy.

However, when adjusted for “organic” transactions—excluding speculative trading—stablecoins still facilitated over US $2.3 trillion in payments, peer-topeer (P2P) transfers, and remittances. Cross-border business-to-business (B2B) transactions on blockchains accounted for a modest US $843 million within this adjusted total, but this segment is expected to grow significantly, with projections indicating a rise to US $1.2 billion by the end of 2024 (Statista). This growth underscores the increasing adoption of stablecoins as enterprises and individuals seek faster, more cost-effective alternatives to traditional cross-border payment systems. As a result, stablecoin adjusted volume of transactions is rapidly catching up to the likes of Mastercard and Visa global networks.

The SAP Digital Currency Hub: Redefining enterprise payments

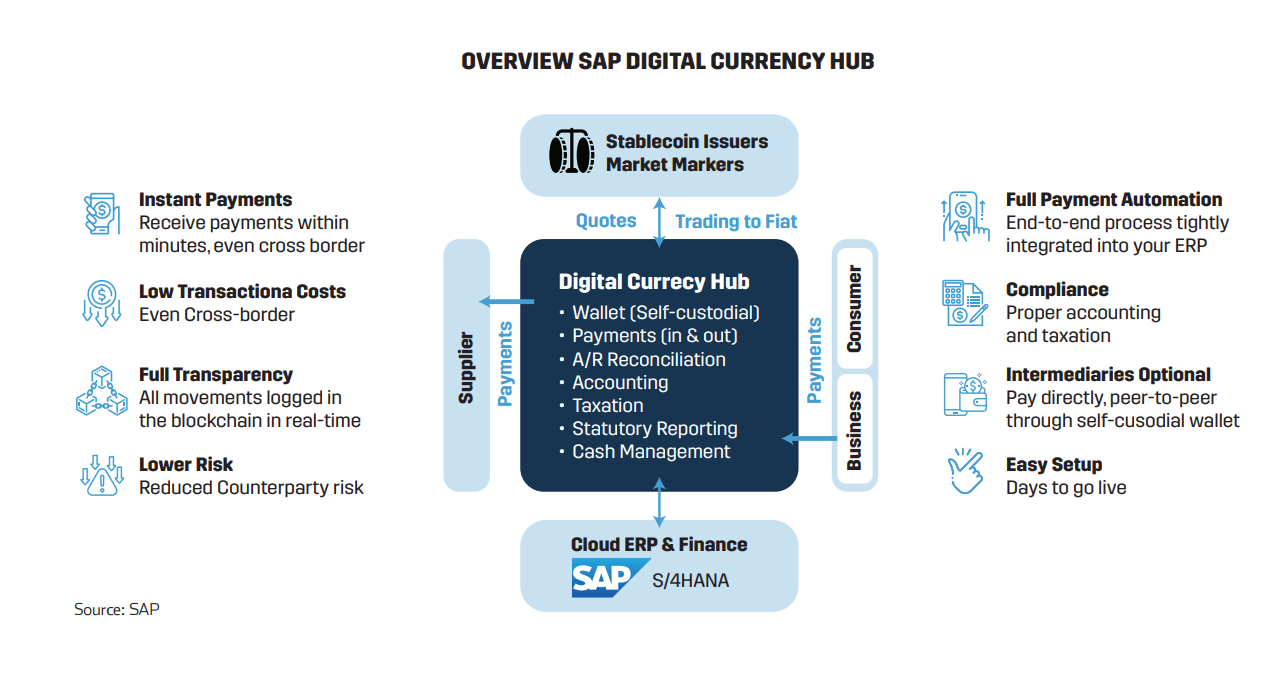

SAP’s Digital Currency Hub is far more than a typical payment platform—it is an enterprise-grade solution designed to seamlessly integrate digital currencies into the financial operations of global businesses. By leveraging stablecoins and blockchain technology, the Hub eliminates inefficiencies in cross-border payments while offering tools tailored to the demands of modern corporations.

Key Capabilities with of SAP Digital Currency Hub

1. 24/7 Instant Payments

The Digital Currency Hub removes the limitations of traditional banking hours, enabling businesses to send and receive payments at any time. This capability ensures smooth operations across time zones, making it particularly valuable for multinational enterprises.

2. Seamless ERP Integration

The platform will directly integrate with SAP S/4HANA Cloud, automating the reconciliation of payments and providing realtime visibility into both fiat and digital currency holdings. This enhanced integration streamlines financial processes, improves cash flow management, and reduces administrative burdens.

3. Multi-Currency and Multi-Network Support

SAP Digital Currency Hub supports leading stablecoins such as USDC and PYUSD, preconfigured for use on blockchain networks like Ethereum and Polygon. Its flexible architecture allows SAPto add additional stablecoins or networks as needed, ensuring adaptability to diverse payment requirements of its customers.

4. Self-Custody Wallets and Fiat Conversion

Businesses can maintain full control of their digital currency holdings through self-custody wallets, eliminating reliance on intermediaries and enhancing security. Alternatively, for organizations that prefer a custody-based model, SAP plans integrations with custody providers to securely store digital assets and manage blockchain transactions through a licensed service provider. The Hub also connects to exchanges for seamless conversions between fiat and digital currencies, simplifying global payment processes.

5. Auditability and Transparency

Blockchain’s inherent transparency provides an immutable record of transactions. This capability significantly reduces fraud risks and facilitates compliance with reporting requirements.

A simplified payment process

To utilize SAP’s Digital Currency Hub, buyers and suppliers first establish a payment agreement specifying the stablecoin and blockchain network for settlement. For example, current options include PYUSD on Ethereum and USDC on Ethereum or Polygon.

1. Invoice Integration

After the payment run, the ERP sends invoices to the Hub. Rather than routing payment instructions to a traditional bank, the Hub processes them for blockchain settlement.

2. Transaction Execution

• If the enterprise opts for self custody, the Hub generates and signs the blockchain transaction directly, allowing the business to retain full control of its digital assets.

• Alternatively, in a custody-based model, the Hub interfaces with custody providers to execute the transaction on the blockchain.

3. Validation and Reconciliation

Once the blockchain transaction is validated and finalized, the Digital Currency Hub generates an account statement, which is uploaded to the ERP system to reconcile payables and receivables.

This streamlined process ensures that stablecoin payments are as intuitive as traditional bank transfers but offer the added advantages of instant settlement, 24/7 availability, and significantly lower fees.

Real-world proof of concept: PayPal, EY, and SAP Collaboration

SAP Digital Currency Hub was recently showcased in the first real-world transaction involving PayPal and Ernst & Young (EY). In September, PayPal used its PYUSD stablecoin to pay an invoice to EY, leveraging SAP’s Digital Currency Hub to facilitate the transaction. The payment, executed on the Ethereum blockchain, was settled instantly and seamlessly integrated into the ERP system for reconciliation.

For PayPal, this transaction highlighted the efficiency and cost-effectiveness of stablecoins in enterprise settings. “The enterprise environment is very well suited for this,” said Jose Fernandez da Ponte, PayPal’s Senior Vice President of blockchain and digital currency. “It’s a very rational conversation to have with the CFO.”

The road ahead: bridging innovation and global payment needs

The SAP Digital Currency Hub demonstrates how digital currencies and blockchain technology can reshape cross-border payments, addressing long-standing inefficiencies such as high costs, delays, and lack of transparency. By integrating these technologies into enterprise systems, businesses can achieve faster, more efficient, and more reliable transactions.

The UAE’s AED Stablecoin initiative adds another layer of relevance, particularly for SMEs and startups in emerging markets. A regulated, dirham pegged digital currency provides these businesses with a stable, cost-effective tool for international and domestic payments while aligning with local regulatory frameworks. When paired with platforms like SAP Digital Currency Hub, AED Stablecoin and similar initiatives enable enterprises to simplify operations, manage cash flow more effectively, and explore opportunities beyond their home markets.

As digital currencies continue to evolve, the focus shifts from experimentation to adoption. For businesses navigating the complexities of globalization, tools that integrate digital currencies into everyday financial processes will become critical. Initiatives like AED Stablecoin—and platforms capable of leveraging them—signal the direction of travel for the future of global payments.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

Darwinbox’s US$140 Million Investment, Co-led by Partners Group and KKR, Set to Accelerate Global Expansion

Darwinbox, a global human resource technology platform, has announced the signing of definitive agreements under which Partners Group, a Switzerland-headquartered global private markets firm, and funds managed by KKR, a US-based global investment firm, will co-lead an investment of US$140 million in the company, with additional participation from India-based Gravity Holdings. The addition of Partners Group and KKR to an already-solid cap-table underscores Darwinbox’s strong momentum over the recent years. The investment positions Darwinbox well to deepen its technology leadership and accelerate its international expansion plans.

Founded in 2015, Darwinbox is a mobile-first and AI-enabled human capital management platform that serves more than 1,000 enterprises around the world. In less than a decade, Darwinbox has expanded internationally across multiple markets, including Asia Pacific, the Middle East, the United Kingdom, and the United States.

In 2024, Darwinbox was recognized as a Challenger in the Gartner Magic Quadrant for Cloud HCM Suites for enterprises with more than 1,000 employees, making it the youngest and only Asian company to receive the accolade.

Since entering the MENA region, Darwinbox has achieved 9X revenue growth over the past three years, building on its local presence through a dedicated regional team that offers in-market support. Many of the region’s marquee brands including Emirates Leisure Retail, DIFC, Lulu, Abu Dhabi Exchange (ADX), Masafi, Salaam Air, WIO Bank among others trust Darwinbox to engage and manage their talent. With full Arabic support on the platform, Darwinbox is also set to launch a pan-GCC multi-country payroll solution this year – further demonstrating its commitment to delivering localized, high-impact HR innovations tailored to the region’s unique needs.

“This investment is a testament to Darwinbox’s strong fundamentals and the trust we have earned from our 1,000+ global customer base,” said Jayant Paleti, co-founder of Darwinbox. “By placing the employee experience front and center — and ensuring our platform is deeply configurable to diverse local needs — we have helped transform HR for enterprises globally. With top-tier investors backing us, we’re poised to amplify our global momentum and deliver innovative AI-powered solutions for thousands of enterprises worldwide.”

On his part, Cyrus Driver, Managing Director, Private Equity, Partners Group, added, “Darwinbox operates in the rapidly growing HR tech market, which we have been tracking through our thematic research. The company is acting as a key disruptor to legacy platforms in this space, investing heavily in product innovation, generative AI, and global expansion, and is well positioned to take market share. We look forward to working with Darwinbox’s talented management team on driving future growth. The company represents another exciting addition to our private equity growth portfolio.”

“Darwinbox has established itself as a leading player in the human capital management space in a short span of time through its focus on innovation and customer centricity,” added Akshay Tanna, Partner and Head of India Private Equity, KKR. “We are pleased to support Darwinbox on its next stage of growth and will look to draw from our global network and expertise to accelerate its international expansion ambitions.”

Globally, over three million employees from leading brands — including Starbucks, Nivea, AXA, Cigna, WeWork, Crisil (an S&P company), T-Systems, and more — rely on Darwinbox’s platform for modern HR management.

Partners Group invested through its growth equity strategy, which applies a thematic approach to identify investment opportunities in growth-stage companies globally. Partners Group made its first growth investment in 2013 and has deployed around USD 2.5 billion in the space to-date. The firm’s recent growth investments include Lumin Digital, a leading cloud-native digital banking provider, and Neara, one of the first AI-powered predictive modeling software platforms for critical infrastructure.

KKR makes its investment from its Asia Next Generation Technology strategy, which seeks to support the growth of innovative, disruptive companies in Asia across consumer technology, software, and fintech. This marks KKR’s latest growth equity investment in India and the region, including Rebel Foods, an internet restaurant company in India; Lenskart, an omni-channel eyewear retailer; Livspace, an omni-channel home interior and renovation platform; KiotViet, a SaaS platform for SMBs in Vietnam; and Privy, a digital trust provider in Indonesia. Avendus Capital acted as the financial advisor and investment banker on this transaction.

Seeking Excellence: Alexander Sysoev, Founder, Great List

Alexander Sysoev, Founder of Great List, is transforming the way diners discover top restaurants with expert-curated recommendations. Now expanding into Dubai, Great List is set to guide both business and leisure diners to unforgettable culinary experiences, offering tailored categories for every occasion—from fine dining to quality casual catch-ups.

In this exclusive interview, Alexander shares his insights into Dubai’s evolving dining scene and how Great List caters to even the most discerning food lovers, surprising them with a selection of venues and experiences unlike anything seen before.

1.Among the many restaurant guides, you chose to focus on the most experienced and demanding gourmets. Why did you take such a challenging path, and how did the idea of Great List come about?

“Great List was born from a desire to find truly outstanding restaurants in every city. Many platforms base their recommendations on mass reviews, paid partnerships, or inconsistent ratings. We saw an opportunity to create something different—an expert-driven guide curated by a team of over 100 individuals with impeccable taste, extensive experience, and complete independence. Most of them are either top executives or business owners—essentially HNWIs with a deep passion for gastronomy. Great List is not just a ranking or a platform with paid listings. It is a carefully curated collection of restaurants that set the highest standards in everything—from cuisine and service to atmosphere and attention to detail. Our audience isn’t just looking for good food; they seek exceptional dining experiences. Our approach is based on quality and independent evaluation. Our team visits restaurants anonymously, pays for their meals, and assesses every aspect—from dish execution to service consistency. If a chef leaves or quality declines, we revisit our recommendations. Unlike traditional guides that update once a year, Great List is dynamic and always reflects the best places at any given moment.”

Source: Great List

Source: Great List

2. Why Dubai? How does its culinary scene compare to other global gastronomic capitals?

“Dubai is one of the most exciting culinary destinations in the world, and it keeps evolving. Unlike cities with centuries-old culinary traditions, Dubai thrives on boldness, diversity, and innovation. Here, dining is not just about food—it’s a full-fledged experience. What sets Dubai apart from other gastronomic capitals is its ambition and versatility. One night, you can dine at a Michelin-starred restaurant, the next, explore local Emirati cuisine, and the day after, enjoy some of the best Indian, Lebanese, or Greek food outside their home countries. Dubai also moves at an incredibly fast pace, with intense competition. Restaurants open and close at a staggering speed, meaning diners are always on the lookout for fresh places and new experiences. This makes Dubai the perfect playground for next-generation guides like Great List, which helps navigate its ever-changing restaurant landscape.”

3. Are chef-driven concepts now taking center stage, or do strong brands remain the key factor?

“Chef-driven concepts are more important than ever, but strong brands still play a role. The key trend is authenticity, storytelling, and a well-crafted customer journey. Modern diners want to know who is behind the kitchen, what inspires them, and why their approach is unique. That’s why we’ve added many extra features to the guide: chef and restaurateur profiles, personal dish recommendations from the chef, as well as tips on dress codes, the best tables to book, and more.”

Source: Great List

Source: Great List

4. How do you see restaurant guides evolving in the future? Are you planning new features or expansion?

“The future of restaurant guides lies in personalization, dynamic recommendations, and rich storytelling. That’s why Great List offers not just convenient categories but also extensive content on finer details that make a dining choice clearer and more informed. We have many new sections in the pipeline, from a calendar of major dining events to the launch of a dedicated hotel guide. In November 2022 we launched the guide in Russia. In January 2025, we launched Great List in Doha (Qatar). We are now exploring expansion into Oman, Kuwait, and Saudi Arabia, as well as considering adding another Middle Eastern country. Simultaneously, we are preparing to launch in Bangkok and Hong Kong, with further plans for Singapore, Almaty, and Baku.”

5. How does Great List help Dubai residents discover new dining spots?

“Great List offers several ways to explore new restaurants. The NEW section highlights places that have opened in the past six months, ensuring our users stay ahead of the latest trends.

Navigating by district helps uncover hidden gems, while browsing by category can lead to unexpected discoveries—such as the perfect spot to impress friends or colleagues. Additionally, getting to know the chefs behind favorite restaurants opens doors to their new projects, offering a gateway to an entirely new world of gastronomic experiences.”

Geidea: Driving Saudi Arabia’s Cashless Revolution in Support of Vision 2030

Though there were several Fintech players active in the Saudi Market prior to 2016, activities were largely unregulated and unsupported by a wider economic infrastructure. Upon the unveiling of the Saudi Vision 2030, several organizations and initiatives were birthed specifically to support the cultivation of the Fintech industry, including the launch of SAMA’s Regulatory Sandbox and CMA’s Fintech Lab, the establishment of Fintech Saudi, a government-backed organization directly mandated to monitor and actively support the development of the Fintech sector.

The Fintech ecosystem has grown rapidly. A cornerstone of this transformation is the country’s shift toward a cashless society, with noncash transactions taking center stage in the modernization of the economy. Among the players shaping this new financial landscape is Geidea, a Saudi-founded Fintech company that has expanded its reach and influence over the past 15 years. Established in 2008, Geidea began with a mission to democratize payment technology and empower businesses, particularly small and medium enterprises (SMEs). Today, it stands as one of the leading Fintech companies in the Kingdom, playing a pivotal role in the broader push for financial inclusion and digital transformation.

Vision 2030 and the goal for a cashless society

Saudi Arabia’s Vision 2030 outlines an ambitious blueprint for economic diversification and modernization, with technology and financial inclusion playing key roles. A central pillar of this transformation is the transition to a cashless society, designed to increase efficiency, enhance transparency, and drive economic activity through digital payments.

In 2016, cash dominated Saudi Arabia’s economy, with only 18% of all transactions conducted electronically. Recognizing the need to modernize, the Saudi government set progressive goals to increase the share of noncash transactions. By 2019, noncash payments had doubled to 36%, reflecting the impact of early regulatory initiatives and the growing adoption of digital payment technologies. The pace of growth accelerated significantly in subsequent years, and by 2023, Saudi Arabia not only surpassed its interim target of 63% but also achieved its 2030 goal of 70% non-cash transactions—seven years ahead of schedule.

Saudi Arabia Vision 2030: Journey Towards a Cashless Society

The Fintech sector has been instrumental in Saudi Arabia’s cashless journey. According to the 2023 Annual Fintech Report, the country is home to 216 operational Fintech companies, representing a vibrant ecosystem that supports the Kingdom’s financial transformation through, for example, infrastructure development. Notably, 33.3% of these Fintechs specialize in payments, underscoring the critical importance of digital transaction technologies.

Under the supervision of the Saudi Central Bank (SAMA), 113 Fintech companies are officially licensed, with 48 operating in payments and finance. This regulatory framework ensures the stability and scalability of the Fintech sector, while encouraging innovation to meet the needs of consumers and businesses that have sifted dramatically. Everyone remembers the COVID-19 pandemic and how it accelerated digital payment adoption across the Kingdom.

Geidea’s Story

In 2008, Abdullah Al-Othman identified a significant gap in the Saudi market: merchants, particularly SMEs, lacked access to affordable and intuitive payment solutions. Recognizing the impending digital revolution, Al-Othman established Geidea to democratize payment technologies, aiming to empower SMEs and foster financial inclusion. The company’s name, derived from the Arabic word for “idea,” reflects its commitment to innovative problem-solving.

Geidea’s mission has been to serve as an enabler for the business environment, reducing the time and costs associated with setting up businesses for small merchants. By leveraging emerging digital technologies, Geidea sought to enhance customer experiences and integrate SMEs into the high-tech ecosystem. Geidea’s early focus was on developing and deploying point-of-sale (POS) systems tailored to the needs of the local market. The company’s first product launched in 2011, but it wasn’t until 2013 when they launched their first certified POS terminal. Within two years, Geidea had captured 50% of Saudi Arabia’s POS market share, becoming a leading provider of payment solutions in the Kingdom.

In 2018, Gulf Capital’s acquisition of Geidea for SAR 1 billion (US $268 million) provided the financial impetus for the company’s expansion. This investment facilitated the enhancement of Geidea’s product offerings and supported its expansion plans. The transaction came just days after the launch of SAMA’s regulatory sandbox designed to foster innovation in the financial sector by providing a controlled environment for Fintech companies and financial institutions to test and develop new products and services.

In March 2021, Geidea, alongside STC Pay, became one of the first non-bank financial institutions to obtain a payment license from SAMA. This authorization enabled Geidea to process payments directly, eliminating the need for traditional banking intermediaries and allowing the company to offer comprehensive payment solutions. In the same year, Geidea became the first in the region to develop an app-based contactless “tap on phone” solution empowering SMEs with a simple way to process customer payments, without a separate payment (POS) terminal or connection.

Building on the momentum of their mobile solution, Geidea formed strategic partnerships with global payment leaders Mastercard and Visa, as well as with the Saudi British Bank (SABB). These collaborations have been instrumental in scaling Geidea’s technologies across the region and expanding its reach in key markets. In 2022, Geidea extended its services to Egypt and the UAE, targeting markets with burgeoning digital economies and substantial SME sectors. Partnerships with institutions like Banque Misr in Egypt and Magnati in the UAE facilitated the localization of Geidea’s offerings.

Geidea’s integration into national systems, such as the National Payments System (MADA), and its participation in SAMA initiatives like QR-code payment standards, further solidified its position within Saudi Arabia’s Fintech ecosystem.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

Tabby: the First Independent Fintech Unicorn in the Middle East

In today’s increasingly tech savvy world, financial solutions must evolve at the pace of consumer needs and Buy Now, Pay Later (BNPL) services have carved a niche, becoming a popular financial model globally due to their flexibility, accessibility, and user-friendliness. These systems address the growing demand for more adaptive financial products that cater to the modern consumer’s desire for immediate gratification while managing budget constraints. They allow shoppers to defer payments without incurring the high costs typically associated with traditional credit options, effectively solving the problem of accessibility to goods with manageable payment solutions.

Since the pandemic, consumer behavior worldwide has undergone a profound shift toward online shopping and digital payment solutions. This change has spurred rapid growth in the popularity of BNPL services, which provide consumers with flexible payment options. The market is experiencing explosive growth, with its global valuation rising from US $156.58 billion in 2023 to an expected $232.23 billion in 2024 — reflecting a CAGR of 48.3%. This surge is fueled by the rapid expansion of e-commerce, rising demand for flexible payment options, and the growing adoption of digital wallets and mobile payments.

By 2028, the BNPL market is forecast to reach $1.015 trillion, driven by the integration of BNPL services in physical retail, cross-border e-commerce, and the rise of embedded finance models. In the Middle East, the BNPL market is poised for significant expansion as regional dynamics create fertile ground for growth. Key factors driving this momentum include a youthful, tech-savvy population, high internet and mobile penetration, and a rapidly expanding e-commerce sector. BNPL services are resonating with Middle Eastern consumers, offering a way to better manage cash flow while enabling immediate access to products and services. For businesses, BNPL solutions have proven to boost customer engagement, drive higher conversion rates, and support long-term revenue growth.

As the demand for BNPL services soars in the Middle East, Tabby has emerged as a pioneering force in the industry. Positioned at the intersection of financial innovation and consumer convenience, Tabby has strategically expanded its footprint to align with this regional momentum, ultimately becoming the first independent Fintech unicorn in the Middle East.

From Founding Vision to Unicorn Valuation

Founded in 2019 by Hosam Arab and Daniil Barkalov, Tabby emerged in Dubai with a mission to transform the retail and consumer finance landscape in the Middle East through accessible BNPL solutions. Hosam Arab, previously the CEO of Namshi, one of the region’s most successful online fashion retailers, brought to Tabby his deep experience in e-commerce and an understanding of Middle Eastern consumers. His cofounder, Daniil Barkalov, leveraged his background in scaling technology at Careem, the region’s ride-hailing leader, where he gained critical insights into building platforms that support rapid growth. Together, they saw a unique opportunity to bridge gaps in financial services and introduce flexible, customer-centered payment options across the MENA region.

Tabby hit the ground running by securing its first seed funding of US$2 million from Global Founders Capital. This initial capital laid the groundwork for building its proprietary technology and assembling a team to execute its ambitious plans.

By 2020, Tabby raised an additional US$7 million in a seed round led by Raed Ventures, followed by a US$23 million Series A led by Arbor Ventures and Mubadala. These rounds enabled Tabby to scale its operations and roll out its BNPL platform beyond Dubai to cover the UAE and Saudi Arabia—two of the region’s largest and most dynamic retail markets. This early expansion cemented Tabby’s position as a key player in the MENA region, empowering millions of consumers to shop with greater flexibility.

A cornerstone of Tabby’s strategy has been forging partnerships with toptier retailers. By mid-2021, Tabby had onboarded more than 2,000 brands, including global names like IKEA, SHEIN, and Adidas, allowing it to cater to diverse consumer needs. The company’s ability to secure these partnerships drove rapid growth, with active users surpassing 400,000 by July 2021. Its Series B funding later that year, led by STV and Global Founders Capital, valued the company at US $300 million and provided the resources needed to scale further.

Tabby’s growth accelerated in 2022 as the company extended its Series B funding to US $54 million and secured US $150 million in debt financing. By August, Tabby had over 4,000 retail partners and 2 million active users. Revenue for the first half of 2022 grew tenfold compared to the previous year.

By May 2023, Tabby had expanded its retailer network to over 15,000 brands and grown its user base to more than 4 million active shoppers. With US $350 million in debt financing and US $58 million raised in a Series C led by Peak XV Partners and STV, the company achieved annualized transaction volumes of US $6 billion. By October 2023, Tabby reported over 10 million users and 30,000 retailer partnerships, solidifying its status as a leader in the Middle East’s BNPL sector.

The pinnacle of Tabby’s journey came in November 2023, when the company closed a US $250 million Series D funding round led by Wellington Management, bringing its valuation to US $1.5 billion and officially joining the unicorn club. Shortly after, Tabby relocated its headquarters to Saudi Arabia, positioning itself at the heart of the region’s most dynamic economy in preparation for its anticipated IPO on the Saudi Arabian Exchange (Tadawul). CEO Hosam Arab described this as “the next logical step” for the company, citing the Kingdom’s strong growth potential and alignment with Tabby’s long-term objectives.

The relocation underscores Saudi Arabia’s central role in Tabby’s strategy, as the Kingdom’s tech-savvy population, dynamic retail sector, and economic reforms under Vision 2030 create fertile ground for innovation and expansion.

In September 2024, Tabby made a strategic acquisition of Tweeq, a Saudi-based digital wallet licensed by the Saudi Central Bank (SAMA). This acquisition marked a shift beyond BNPL, integrating digital banking capabilities to offer more comprehensive financial solutions.

Tweeq’s digital spending account aligns with Saudi Arabia’s National Fintech Strategy and Vision 2030, which aim to drive financial inclusion and promote a cashless economy.

By late 2024, Tabby’s user base has grown to over 14 million, with a network of more than 40,000 retailers and small businesses. As Tabby prepares for its IPO, it stands as one of the Middle East’s most prominent Fintech success stories, poised to reshape the region’s financial landscape while contributing meaningfully to Saudi Arabia’s ambitious Vision 2030 goals.

What does the future hold for Tabby?

With a planned IPO on the Saudi stock exchange, Tabby is set to become one of the few Fintechs in the region to go public locally. Going public will provide Tabby with access to new capital, enabling it to scale operations, fuel product innovation, and attract institutional investors seeking exposure to the Middle East’s booming Fintech sector.

But Tabby’s ambitions are extending far beyond its roots in BNPL services. The company is on a mission to become a multi-faceted financial services platform. Key to this strategy are recent acquisitions and new product offerings such as the Tabby Card for in-store purchases and the Tabby Shop digital shopping assistant. These initiatives demonstrate Tabby’s drive toward creating a seamless, omnichannel payment experience. As the region embraces embedded finance, Tabby is well-positioned to integrate its services into broader shopping and financial experiences, offering consumers more personalized payment options and frictionless purchasing journeys. Over time, this strategic expansion could even position Tabby as a contender in the emerging “superapp” space, where a single platform offers users a suite of financial, shopping, and lifestyle services.

By embedding itself into essential consumer spending habits and diversifying its product offerings, Tabby is redefining its role in the Middle East’s financial services ecosystem. The company’s efforts to expand its range of services, enhance customer engagement, and solidify its market leadership are paving the way for sustained growth. As Tabby prepares for its IPO and continues its transformation into a multi-service financial platform, it is clear that the company’s influence will extend far beyond BNPL. With a growing customer base, diversified revenue streams, and a foothold in Saudi Arabia’s rapidly growing Fintech market, Tabby is poised to lead the next wave of financial innovation in the Middle East.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.#

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

10 Graphs You Need to See About Fintech in the Middle East

Fintechs have been bubbling up the world over, and their strong foothold in the Middle East is no exception. What might come to the surprise of many, is just how strong and diverse the regional Fintech landscape is, how much financing regional players are attracting, how many Fintech unicorns the region is producing, and just how well it measures up against global heavy-weight Fintech nations like the US and the UK.

Check out these 10 graphs to put it all into perspective for you.

1. Who’s Producing the Majority of the World’s Fintech Startups?

The United States produces the most Fintech startups in the world, with over 42,500 Fintechs calling it home. It’s no surprise though, when you take a look at how many tech startups across all sectors the US produces, which hovers at around half a billion. We must also consider how many people around the world register their tech startups in the US, despite being based elsewhere for regulatory or other reasons.

The second largest producer of startups and home to techpreneurs is the United Kingdom, with nearly 100,000 tech startups, of which over 10,230 are Fintechs. When compared to the US, though, the UK’s 2nd place is just a quarter of the size. When we look at well-funded Fintechs, or scale-ups (which are defined as startups that have successfully raised US $1 million or more), American Fintech scaleups outnumber UK Fintech scallops 5 to 1.

One might make an argument for America’s population of over 335 million people producing more startups than the UK’s nearly 70 million inhabitants, just a question of the baseline population of any ecosystem – but India’s population of 1.4 billion people, lags far behind in 3rd place, with half as many Fintechs as the UK. The infobyte below also indicates GDP per capita to add as a variable – where India lags far behind its counterparts, but still manages to produce significantly more Fintech scale-ups that are well-funded than Germany, Canada, France or Australia.

2. Middle East Often Outpaces America in Fintech Adoption

If the United States produces the most Fintechs in the world, one might expect it also to be a country that has high Fintech adoption rates, and it certainly does fall into the top quartile. That said, top Middle Eastern countries like the United Arab Emirates, Saudi Arabia, Turkey and Israel also have high Fintech adoption rates, largely on par with the USA or in many cases, outpacing American adoption.

For example, more Saudi Arabians use mobile payment services than Americans, which have mobile payment adoption rates on par with the United Arab Emirates. More Turkish and UAE residents own cryptocurrency than Americans do. More Turkish and Israeli people use a website or mobile app to do their banking, investment or insurance acquisition than Americans do.

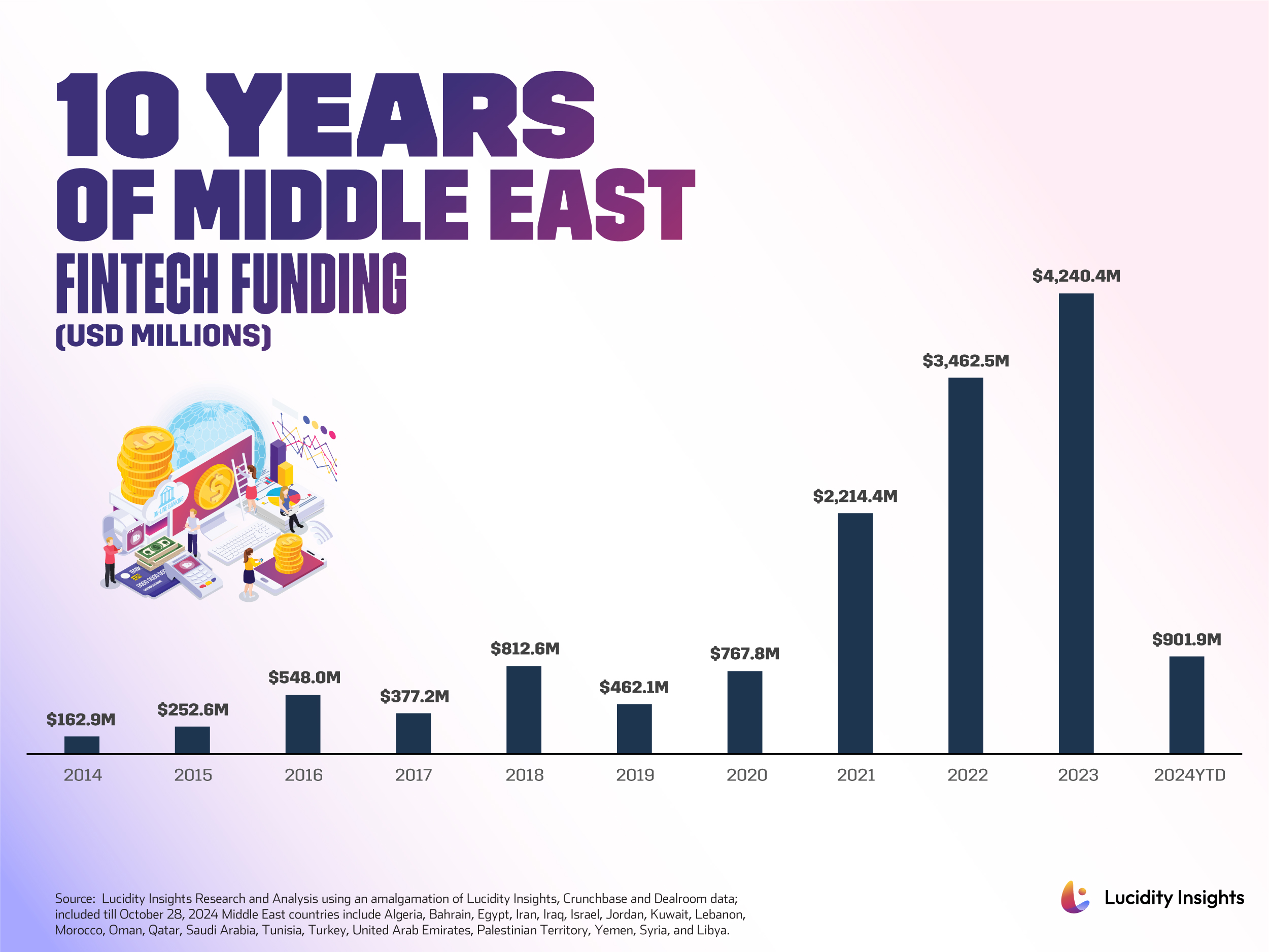

3. Fintech Funding in the Middle East Peaked in 2023 at US $4.2 Billion

Fintech funding peaked in the Middle East in 2023 at US $4.2 billion, before various factors influenced a downturn in 2024 including a global VC Winter which started to take hold in 2023 and continued its icy grip on fundraising purse-strings across the world into 2024. Israel’s War on Gaza has also affected a previously strong tech sector in Israel – which has slowed considerably since the bloodshed began on October 7, 2023.

Israel currently faces an uncertain political and economic future. Though large cybersecurity firms and established incumbents are still attracting US $100 million plus mega-rounds, much of the seed capital has dried up for newer startups trying to establish themselves. Despite the headwinds facing Israel though, in 2024, 7 out of 26 of the Fintechs that raised a US $100 million+ megaround in the MENAPT region were based out of Tel Aviv, which accounts for 27%.

4. MENA: Home to 26 Fintech Soonicorns

There are 26 Fintech soonicorns in MENA, if fundraising US $100 million or more is of any indication. Fourteen out of the 26 soonicorns (27%) are Israel-based, having raised over US $3.1 billion collectively over their lifetime. Four Saudi Arabian Fintechs have also fundraised over US $3 billion collectively, showcasing how valuable Saudi Fintechs are at present, and how much more valuable they are than Israeli or UAE Fintechs (If you’re wondering why this is the case, it’s likely based on simple demographics. The UAE and Israel cater to just over 10 million people, while Saudi Arabia’s population is nearly 4 times that).

Four Fintech startups based in the United Arab Emirates have collectively raised over US $1.67 billion as well. There are also startups from Egypt, Bahrain, and Algeria on the list, with Fintechs in payments raising the most capital, at 41% of US $9.3 billion collectively raised by these 26 regional soonicorns. Superapps, wealth and investment startups, and lending startups are the top Fintech sub-sectors that have collectively raised the most funding out of the soonicorn pool, coming in behind startups in the paytech, money transfer and remittances space.

5. Here are MENA’s Most Funded Fintech Startups of All Time (2024)

The Top 20 most funded Fintechs in MENA span quite the fundraising range from Egypt’s Fawry raising US $122 million before IPO-ing in 2019, to the UAE-born, KSA-based, Tabby, who has raised over US $1.7 billion thus far and is rumoured to be preparing for its own IPO. Both are valued at over US $1 billion, but have raised starkly different figures to get to that coveted inner circle of Middle Eastern born unicorns.

There are also some cross-over Fintechs on this list, such as Careem, which was considered a mobility player, before it moved into remittances and wallets to become a regional SuperApp play. Foodics has traditionally been considered more of a foodtech or restaurant SaaS play, though its restaurant financing product has helped it venture more concretely into the Fintech space. Many of the region’s unicorns are on this list, and the rest we should keep a close eye on, as the next big unicorn is likely on this list too.

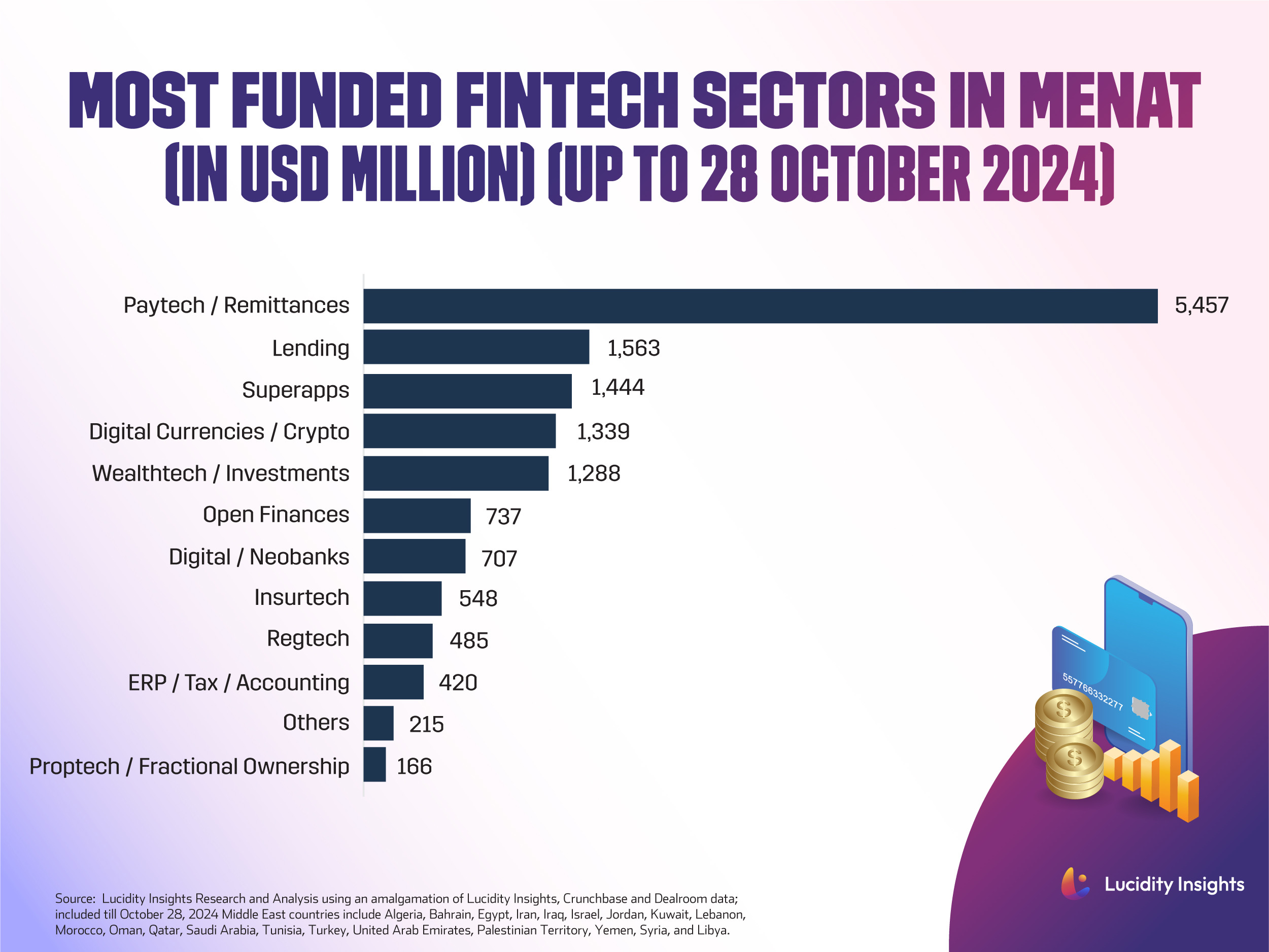

6. Most Funded Fintech Sector in MENAT to Date

As is the case in most parts of the world, Paytech, or tech startups in the payments and remittances space have been most largely funded in the MENAT region, accumulating over US $5.4 billion in funding over the last 20+ years since Fintechs began entering the Middle East scene. But as the region’s startups are getting more advanced, fundraising figures are fast catching up, with Lending, SuperApps and Digital Asset or Crypto and Wealthtech startups fundraising and attracting large swaths of capital too.

7. MENA Macro VC Investment Trend by Startup Growth Stage and Country (2018-2024 YTD)

This would be considered the ‘Data Dump Goldmine’ that helps us understand the maturity of different Fintech markets, and key trends across the highest performing Middle East markets over the past six to seven years. It tells us that in early stage Fintechs, average funding deal sizes have increased over time across all key markets in the Middle East. For growth stage funding rounds, different countries have peaked deal sizes at different times – but most saw 2023 as a highlight year.

Late stage investments vary across the board, as Israel has an older, more developed sector, while some key UAE-based later-stage Fintechs have opted to move headquarters to KSA to attract financing and seek out IPO exits. Egypt and Turkey seem to be in too early its startup ecosystem development to have any late stage Fintech funding rounds, showing us that every country has a different definition to “nascent stage”.

8. UAE is home to the Most Fintech Scaleups in the Middle East

The UAE is home to the most Fintech scaleups at 155 that have raised over US $1 million or more. That’s more Fintech scaleups than Israel, which is quite the feat – as Israel is known to be a Fintech and cybersecurity powerhouse – not just in the region, but across the World. Of course quality is more important than quantity, but as many Fintechs around the world (including Israeli Fintechs) move headquarters to Dubai, there is something brewing there.

But it’s not a landslide victory for the UAE Fintech scene; Israel follows close behind at 141, then Turkey, Egypt, and Saudi Arabia follow in the distance, rounding out the top 5 markets producing Fintechs that have been backed by substantial investor cash – with 41, 46 and 47 Fintech scaleups each, respectively. The UAE’s ease of doing business, English business language, globalized and international workforce, and transparent financial regulatory infrastructure is likely key reasons as to why it’s home to more successfully fundraised Fintech startups than any other country in the region.

9. 66 Fintech Exits in the Past Six Years

There have been 66 exits in the Middle East and Turkey Fintech space over the past 6 years, of which only 7 were IPOs. Acquisitions and Buyouts is the main off-ramp for startups in the region, of which Israel has had the most exit success, with 29 exits since 2018; rounding out the top 3 markets is the UAE and Turkey, which had 15 exits and 14 exits, respectively. Israel, UAE, and Egypt are the only markets that have had Fintech startups successfully IPO over the years.

10. Top Fintech Investors in MENAT

The region is rich in Fintech investors, whether they are incubators and accelerators or venture capitalist players investing in the Middle East, Africa and Turkey’s Fintech scene from here or abroad. Of course, incubators and accelerators that have set themselves up regionally – players like 500 Global, Techstars, Plug and Play, and Flat6Labs tend to have higher investment numbers by the nature of their structure, and the volume of startups going through their programs annually. Even Silicon Valley’s Y-Combinator has made 30 investments in Middle East Fintechs amounting to over US $250 million collectively over the past 6+ years.

When we look at all investments made from 2018 to Q3 2024, the heaviest hitter for regional Fintech investments is STV out of Saudi Arabia, who has invested over US $924 million across 16 regional Fintechs; this comes as no surprise, as STV is one of the few later stage investors in the region, investing only in startups that are at the Series B stages or higher which always has larger ticket sizes.

Abu Dhabi’s Shorooq Partners follows close behind STV with US $879 million invested across 24 regional Fintechs largely across Seed to Series A cheques. Dubai’s MEVP falls in a distant 3rd place, when you look at investment amounts at US $374 million across 17 Fintech deals, as a largely growth stage investor in the Series A category.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

The State of Fintech in 2024

The Financial Technology (Fintech) sector has transformed from a disruptive niche into a cornerstone of global finance. As of September 2024, the industry boasts a combined market capitalization of US $851.9 billion, marking a 41% rise since 2019. Despite recent market recalibrations, the sector’s long-term trajectory remains strong, underpinned by 576 Fintech unicorns collectively valued at US $2.2 trillion. Here we examine the key drivers behind Fintech’s rapid ascent, profiling the leading players, and analyze the evolving investment landscape that will shape its future trajectory from a global lens.

Rewiring Finance: Fintech’s Evolution and Market Power in 2024

Over the past two decades, the Fintech sector has evolved from a niche player into a disruptive force, fundamentally reshaping global financial services. Initially seen as an alternative to traditional banking, Fintech has now become integral to multiple areas of finance, including payments, lending, digital currencies, insurance, and wealth management. This transformation has been driven by rapid technological advancements, shifting customer preferences, and strong support from investors and regulators. As Fintechs continue to introduce innovative, customer-centric solutions, they are not only meeting the evolving demands of modern consumers but also setting new standards for efficiency, accessibility, and personalization in financial services.

As of September 2024, publicly traded Fintech companies hold a combined market capitalization of US $851.9 billion, a 41% increase since 2019. However, this marks a significant drop from the US $1.4 trillion peak achieved in 2021, reflecting a market correction primarily driven by the ‘new normal’ of a high-interest environment. Despite this setback, the industry’s long-term growth remains promising, with 576 Fintech unicorns globally, collectively valued at US $2.2 trillion—a threefold increase from five years ago when only 187 firms had reached unicorn status.

Top 5 Most Valued Global Fintechs in 2024

The top five most valuable fintech companies are industry leaders in payments, digital banking, and blockchain, boasting multi-billiondollar valuations. PayPal, the oldest among them, capitalized on the internet boom of the late 1990s and early 2000s. Over the past 25 years, PayPal has continuously innovated, establishing itself as a global leader in online payments, operating in most countries that support digital money transfers. Paypal IPOed in 2002.

Close behind is Stripe, founded in 2014, another major player in the payments space, with a valuation of US $70 billion as of September 2024. Stripe holds the distinction of being the highest-valued privately-owned Fintech in the world, having raised a total of US $8.7 billion in funding. It also ranks among the top five most valuable privately held companies globally. Stripe made headlines in January 2023 with speculation about its plans to go public. However, as of November 2024, the company has not confirmed any intention to do so. Instead of pursuing a public listing during an election year, Stripe opted to provide liquidity to its current and former employees. This was achieved through a US $694.2 million tender offer funded by existing investors and a stock buyback by the company itself.

In the third and fifth positions are two neobanks— Nubank and Revolut—which have emerged as compelling alternatives to traditional banks. These digital-first banks have experienced explosive growth, offering innovative financial services to millions of users worldwide, challenging the dominance of conventional banking institutions.

Ranking fourth is Binance, the world’s largest cryptocurrency exchange. Since its launch in 2017, Binance has leveraged the growing blockchain and cryptocurrency market to achieve a US $62 billion valuation, solidifying its position as a key player on the Fintech landscape.

Venture Capital’s Role in Fintech Growth

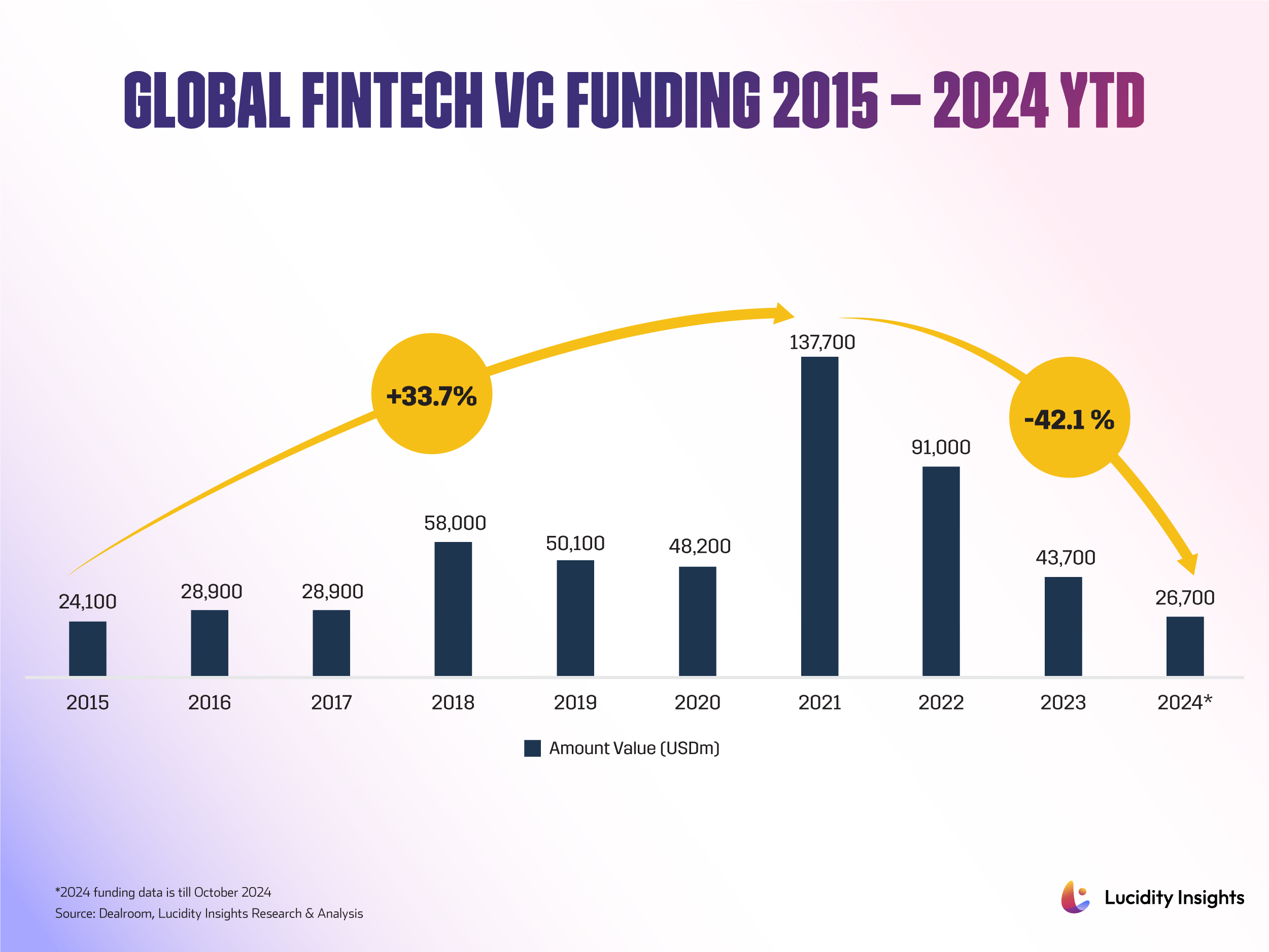

Venture Capital (VC) funding has played a crucial role in Fintech’s impressive growth trajectory, particularly from 2015 to 2021. Over this period, funding surged at a compound annual growth rate (CAGR) of 33.7%, climbing from US $24.1 billion in 2015 to a peak of US $137.7 billion in 2021. This rapid expansion was largely due to accelerated digital adoption during the COVID-19 pandemic and favorable economic conditions, where abundant liquidity and low interest rates encouraged investors to fund innovation.

However, the landscape has since shifted markedly. As global interest rates rose, a “VC Winter” set in, with funding becoming more conservative and selective. The shift in priorities has seen investors gravitating toward larger, established Fintechs to strengthen market consolidation rather than taking on the risk of funding numerous early-stage startups. By 2023, Fintech funding had fallen to US $43.7 billion. As of October 2024, the year-to-date funding stands at US $26.7 billion, reflecting a notable decline with a negative CAGR of –42.1% from the 2021 peak.

Despite the reduced funding levels, Fintech has maintained its position as one of the top three most funded startup sectors globally over the past decade behind health and enterprise software. This underscores the sector’s enduring relevance and the continuing investor interest, even amidst economic headwinds.

Fintech is now integral to the future of financial services, offering innovative solutions that address both consumer and enterprise needs. While payments, lending, and banking remain at the core of Fintech’s disruption, adjacent sectors like Insurance Technology (InsurTech), Regulatory Technology (RegTech), and wealth management are also undergoing significant transformation. Furthermore, the convergence of digital currencies, blockchain technologies, and Decentralized Finance (DeFi) underscores the expansive potential of Fintech, pushing it beyond the traditional boundaries of banking.

Key Subsector in Fintech

A key catalyst for Fintech’s growth has been its close correlation with the rise of e-commerce. As digital marketplaces have expanded, so has the demand for seamless payment systems, buynow-pay-later (BNPL) options, and accessible lending platforms. Fintech solutions serve as the infrastructure backbone for these services, facilitating frictionless transactions, cross-border payments, and consumer credit, particularly in regions where traditional banking systems have struggled to keep pace with the rapid digitization of commerce. This symbiotic relationship has propelled Fintech to become one of the most heavily funded sectors in tech across various regions. In many emerging markets, Fintech is often the first sector to produce unicorns, reflecting its critical role in driving economic innovation.

Future Prospects for Fintech

Despite recent market fluctuations, Fintech’s fundamentals remain robust. The sector sits at the intersection of several long-term shifts, including the ongoing digitization of financial services, the rise of embedded finance (integrating financial services into non-financial platforms), and greater regulatory openness to innovations like open banking and AI-driven financial products. These developments position Fintech for sustained growth, even in the post-pandemic environment where investors are more focused on sustainable, profitability-driven ventures.

McKinsey & Company projects that Fintech industry revenues will grow nearly three times faster than those of traditional banking from 2022 to 2028. While traditional banking revenues are expected to increase at an annual rate of 6%, Fintech is set to achieve an impressive 15% annual growth, potentially reaching a net revenue range of US $325 billion to $463 billion. This growth trajectory underscores Fintech’s rising influence and resilience within the shifting financial landscape.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

The Rise of Middle East Fintech: Unicorns, Investments, and Regional Growth

Fintech continues to dominate the world’s tech ecosystems, and fintech startups have attracted well over half a trillion dollars in venture capital investing in the last decade from 2015 to 2024. Global fintech VC investment peaked in 2021 with US $137.7 billion worth of funding distributed in a single year.

Furthermore, at least three of the top ten most valuable privately owned companies in the world are fintechs (as of the end of 2024) – namely, Ireland-based payments player Stripe (US$70 billion valuation), UK-based Neobank Revolut (US$45 billion), and US-based Neobank Chime (US$25 billion). If you count crypto-exchanges as Fintechs, as we do in this report, then we would have to make room for Binance (US$62 billion) and Coinbase (US$47.5 billion).

Despite this list being dominated by western startups, there are emerging market leaders too. Ant Group, which is the parent company of AliPay – one of China’s largest digital payment providers serving 1.3 billion users and 80 million merchants – is valued at US$80 billion. Nubank, a Brazilian Neobank with a staggering US$56.4 billion valuation has over 100 million customers across key South American countries, is profitable, and successfully IPO’d in 2021.

Middle East Fintech Unicorns: Pioneers of the Region

Though valuations of regional MENA fintechs are much smaller, many of the region’s first wave of unicorns have been fintechs as well. UAE-born, KSA-headquartered Buy-Now-Pay-Later (BNPL) player Tabby, reached unicorn status at the end of 2023 when it raised US$200 million at a US$1.5 billion valuation. Other fintech unicorns in the region include Turkey’s Papara (US$1.5 billion), Egypt’s MNT-Halan (>US$1 billion), and Saudi Arabia’s Tamara (>US$1 billion). There are many up-and-coming soonicorns in the region as well, with the likes of Geidea, Midas, PayTabs and Sarwa all making waves. 26 MENA-based fintech startups have successfully raised over US$100 million, also indicating a strong line-up of companies vying for unicorn-status in the coming years.

Middle East fintech funding peaked in 2023, with US$4.2 billion worth of funding raised by fintech startups, seemingly unaffected by the VC winter until a marked drop came in 2024. Though there are many reputable local and regional Venture Capital investors, there are also many international investors that have looked to support startups from the region. One such indicator is Y-Combinator’s (YC) growing pool of Middle Eastern Fintech alumni; to date, YC has invested in 30+ Fintechs from the MENA region.

Related: New Report Highlights the Middle East as a New Global Fintech Contender

Sector Spotlight: Payments, Crypto, and Wealthtech Innovations

Across the region, over 5,450 funding rounds have been made out to payment and remittance fintech startups, accumulating over US$5.4 billion in investments over the years. Fintech companies that are developing lending, superapps, crypto and wealthtech solutions are all heavily invested in sectors as well.

It can be estimated that there are roughly 2,000 fintech startups across the MENAT region, of which half are likely to have raised some form of capital and disclosed it. Of this group, 465 have successfully raised US$1 million or more, reaching scaleup status. Though Israel has the highest number of general technology scaleups calling it home, the UAE has the highest number of fintech scaleups, with most residing in Dubai. This speaks to the UAE being a regional financial hub with a national fintech strategy in place. Other countries in the region that are rapidly developing their fintech sectors include Saudi Arabia, Turkey, and Egypt. We hope you enjoy this informative special report, on the state of fintech in the Middle East.

Explore the transformative trends shaping the Middle East’s Fintech sector. Read or download your copy of “The State of Fintech in the Middle East” now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa’s tech and entrepreneurial ecosystems.

These Five Lessons from the World of Broadcasting Could Boost your Business Communication

This article was co-written with Louisa Preston.

Clear and confident communication is one of the biggest challenges in business. In a recent a recent report by Bayt.com by Bayt.com, poor communication was identified as the primary obstacle to leadership effectiveness. As an expert in a particular field, there is often a tendency to over-complicate a message. But as journalists, we quickly learnt that less is more; the key to success is to do the hard work before you start speaking and distill your information to make it easy for the audience to absorb. By communicating with impact, it is amazing how much you can convey in just 30 seconds.

Effective communication is not simply about structuring your content in an accessible way, it is also about delivering with confidence and impact. We often hear from women in business that they lack the confidence to speak up, particularly in male-dominated industries, which presents a barrier to female leadership development.

Drawing on our experiences of broadcasting live in high-stakes moments, there are some practical techniques that can help both women and men to communicate more effectively in business. Whether you’re delivering an executive presentation, pitching a business idea, or talking to the media, what you say and how you say it can make or break the opportunity.

- Create a clear structure Telling a story is the key to engaging your audience and making your message memorable. Every story needs a beginning, a middle and an end, and this is a good way to structure your presentation. Repeating your core message at each stage will help it stick, and using practical evidence or data to reinforce your ideas will add authenticity to your words.

- Open with a hook An intriguing opening will enable you to capture your audience straight away. Start out with something original and thought-provoking that grabs attention and inspires curiosity. The hook is your first opportunity to win (or lose) an audience.

- Use your body language Your physical presence and body language play a vital role in confident communication. Use your movements to establish a balance that creates energy in the room, without being distracting, and try to make eye contact across each segment of the audience. Professionals will often adopt a strong stance with feet shoulder width apart or even create an entire alter-ego to feel more confident and in control.

- Vary your vocals Vocal variation is also critical to keeping your audience engaged. Adjust your tone, modulate your pace and use pauses for impact at the relevant moments. Make primary points with ‘verbal signposting’ to help the audience identify the important takeaways.

- Close with impact At the end of a presentation you want to leave the audience with food for thought. Reiterate your core message and end with an impactful statement or call to action that will encourage a continuation of conversation.

As broadcasters we have experienced nerve-wracking moments of presenting to millions of people. Thinking more about you audience and how you want them to feel listening to you and how your messages would land better for them is the key to harnessing your confidence and becoming a better presenter. Taking control of what you are saying, and getting your message across more effectively, you will find that you can deliver successfully in those high-stakes moments, irrespective of how you feel internally.

Rebiha Helimi’s RH Élite Club Debut Marks a New Chapter for the Economic Growth of Souk Ahras, Algeria

Rebiha Helimi has introduced the RH Élite Club in Souk Ahras, Algeria, as a multi-functional complex ultimately aimed at propagating commerce through its modern spaces for dining, vitality, and community interaction. It included a restaurant, an ice cream parlor, a health and fitness boutique, a fully equipped gym, and a dedicated boxing facility. All of these were for the purpose of providing an experience of accessible luxury.

The launch event at the Sheraton Annaba in Algeria featured standout performances including from Cheb Momo, Cheba Zahouania, and Kenza Morsli. Influential guests added further high-octane energy, including Salima Souakri, the country’s judo icon; Mehdi Baghdad, professional boxer; Doria Khetib and Meriem Ammam, social media figures; Imen Noel, fashion and beauty influencer; and Melissa Sahouni, Miss Africa. Belkisse Turqui hosted the event.

Related: RH Luxury Properties Boss Rebiha Helimi Launches Plans to Link Dubai and Africa Real Estate

With the launch complete, the RH Élite Club now operates as an idyllic setting where everyone can play an active part in supporting the overall long-term development of Souk Ahras, Algeria.

Related: The 100: Rebiha Helimi, Founder and CEO, RH Luxury Properties